Anúncios

In the dynamic landscape of personal finance, your credit score stands as a pivotal indicator of your financial health and reliability. For residents of the United States, a strong credit score is not merely a number; it’s a gateway to favorable interest rates on loans, competitive insurance premiums, easier apartment rentals, and even certain employment opportunities. As we look ahead to 2026, understanding the core components that shape your US Credit Score Factors becomes more critical than ever. The methodologies behind credit scoring are constantly refined, and staying informed is your best defense against financial setbacks and your most powerful tool for unlocking financial advantages.

This comprehensive guide delves deep into the five most impactful factors influencing your US credit score in 2026. We’ll break down each element, explain its significance, and provide actionable strategies to help you optimize your score. Whether you’re aiming to buy a home, finance a car, or simply improve your financial standing, a thorough understanding of these factors is indispensable. Prepare to embark on a journey that will demystify your credit score and empower you with the knowledge to build a robust financial future.

Anúncios

Understanding the Foundation: What is a US Credit Score?

Before we dissect the individual factors, it’s important to grasp what a US credit score truly represents. In essence, it’s a numerical expression of your creditworthiness, derived from the information contained in your credit report. The two most widely used credit scoring models in the US are FICO (Fair Isaac Corporation) and VantageScore. While they share many similarities, their exact methodologies and weighting of factors can differ slightly.

Your credit score serves as a quick snapshot for lenders, allowing them to assess the risk associated with lending you money. A higher score indicates a lower risk, often leading to better terms and easier approval for credit products. Conversely, a lower score suggests a higher risk, potentially resulting in higher interest rates, stricter loan requirements, or even outright denial of credit.

The average FICO score in the US typically hovers around the high 700s, with a range generally from 300 to 850. VantageScores also range from 300 to 850. Understanding where your score falls within this spectrum is the first step toward effective credit management. But knowing the number isn’t enough; you need to understand the levers that move that number, which brings us to the core US Credit Score Factors.

Anúncios

Factor 1: Payment History – The Bedrock of Your Creditworthiness

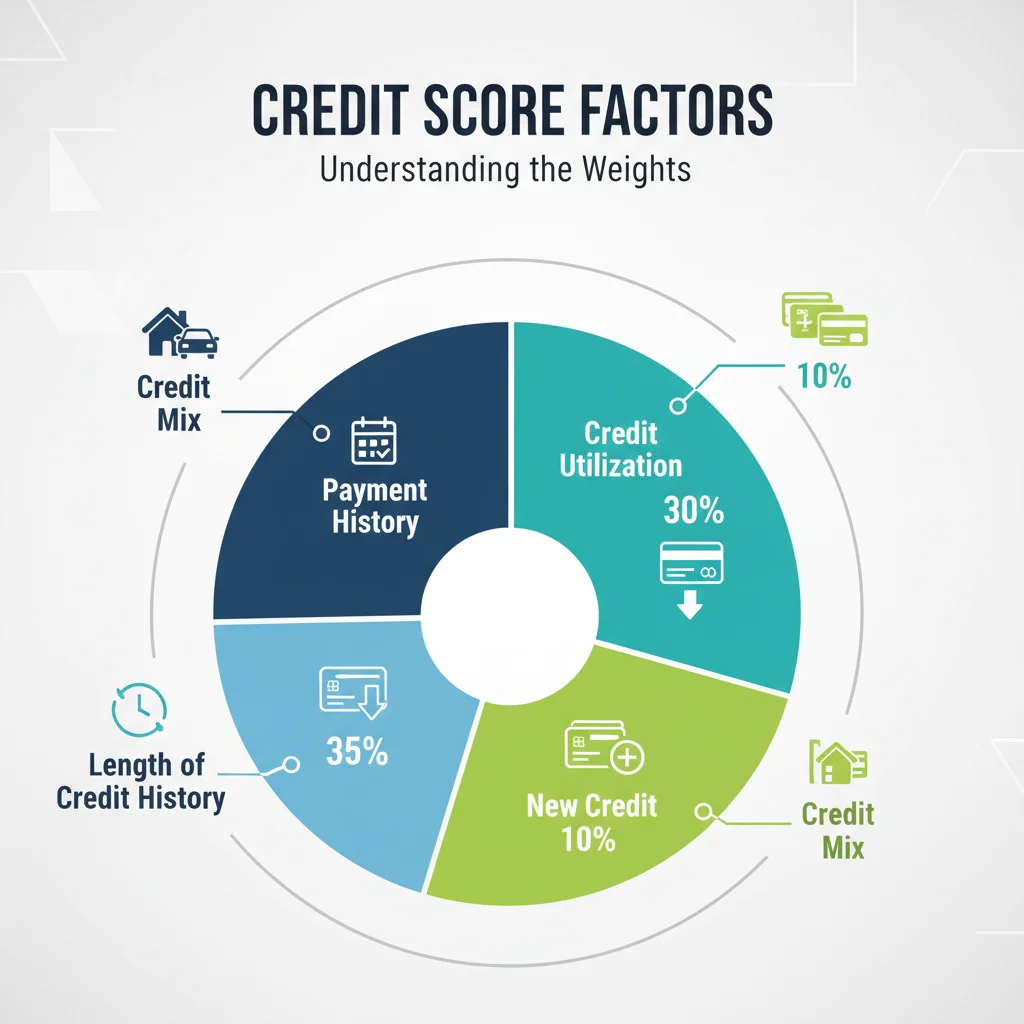

Without a doubt, your payment history is the single most influential factor affecting your US credit score. It typically accounts for a substantial portion of your score – around 35% for FICO scores. This factor reflects your track record of paying your debts on time. Lenders view past payment behavior as a strong indicator of future payment behavior. Consistently making on-time payments demonstrates reliability and financial responsibility, signaling to lenders that you are a low-risk borrower.

What Constitutes Payment History?

- On-time payments: Every payment made by its due date contributes positively to your score.

- Late payments: Payments that are 30, 60, 90, or more days past due can severely damage your credit score. The longer the delay and the more frequent the late payments, the greater the negative impact.

- Public records: Bankruptcies, foreclosures, and tax liens are considered major derogatory marks and can devastate your score for many years.

- Collections: Accounts sent to collection agencies also have a significant negative impact.

Why is it so Important?

Imagine you’re lending money to a friend. Wouldn’t you want to know if they’ve consistently paid back previous loans on time? Lenders operate on the same principle. A spotless payment history is the clearest signal of your ability and willingness to meet your financial obligations. Even a single late payment can cause a noticeable drop in your score, and multiple late payments can be catastrophic.

Strategies for Optimizing Payment History:

- Pay on time, every time: This is non-negotiable. Set up automatic payments, calendar reminders, or use budgeting apps to ensure you never miss a due date.

- Prioritize: If you’re facing financial hardship, prioritize minimum payments on all accounts over paying one account in full and missing others.

- Communicate with creditors: If you anticipate difficulty making a payment, contact your creditor immediately. They may be willing to work with you on a payment plan or offer temporary relief, which is far better than a missed payment reported to credit bureaus.

- Review your credit report: Regularly check your credit report for inaccuracies. If you find any late payments or derogatory marks that are incorrect, dispute them immediately with the credit bureau.

Factor 2: Credit Utilization – The Art of Responsible Borrowing

The second most influential factor, typically accounting for about 30% of your FICO score, is credit utilization. This refers to the amount of credit you’re currently using compared to the total amount of credit available to you. It’s often expressed as a ratio: (total credit used / total credit limit) * 100%. A low credit utilization ratio indicates responsible borrowing and is a strong positive signal to lenders.

Understanding the Ratio:

If you have a credit card with a $10,000 limit and you currently owe $2,000 on it, your utilization for that card is 20%. If you have multiple cards, the credit scoring models look at both individual card utilization and your overall utilization across all revolving accounts.

Why Does it Matter?

A high credit utilization ratio suggests that you might be over-reliant on credit or struggling financially. Lenders perceive this as a higher risk. Conversely, maintaining a low utilization ratio demonstrates that you can manage credit responsibly without maxing out your available lines. The general rule of thumb is to keep your overall credit utilization below 30%, and ideally even lower, closer to 10% for the best scores.

Strategies for Optimizing Credit Utilization:

- Keep balances low: Pay down your credit card balances as much as possible, ideally before your statement closing date.

- Increase credit limits: If you’re a responsible borrower, you can request a credit limit increase from your credit card issuer. This increases your available credit without increasing your debt, thereby lowering your utilization ratio. However, only do this if you trust yourself not to spend the additional credit.

- Avoid closing old accounts: Closing an old, unused credit card can actually hurt your utilization ratio, especially if it has a high credit limit. This is because it reduces your total available credit, potentially increasing your ratio even if your debt remains the same.

- Pay multiple times a month: Instead of waiting for your statement to close, consider making several smaller payments throughout the month to keep your reported balance low.

Factor 3: Length of Credit History – The Value of Time and Experience

Often referred to as “age of credit,” the length of your credit history typically accounts for about 15% of your FICO score. This factor considers how long your credit accounts have been open and the average age of all your accounts. A longer credit history, especially one with a consistent record of responsible borrowing, is viewed favorably by lenders because it provides more data points to assess your long-term financial behavior.

What Does it Measure?

- Age of your oldest account: The longer your oldest account has been open, the better.

- Age of your newest account: A very new account can slightly lower the average age of your accounts.

- Average age of all accounts: This is a key metric.

Why is Longevity Valued?

Think of it like a resume. An employer is more likely to trust a candidate with a long, consistent work history than someone with a very short one, even if that short history is spotless. Similarly, a lengthy credit history provides lenders with a comprehensive view of your financial habits over time, reducing uncertainty about your ability to manage debt responsibly.

Strategies for Optimizing Length of Credit History:

- Start early: The sooner you open your first credit account (responsibly, of course), the sooner you begin building a long credit history.

- Keep old accounts open: Even if you don’t use them frequently, keeping old, active accounts open and in good standing helps maintain a long average age of accounts. Just be sure to use them occasionally to prevent them from being closed by the issuer due to inactivity.

- Be mindful of new accounts: While new accounts are necessary for growth, opening too many in a short period can lower your average account age.

Factor 4: New Credit – The Impact of Recent Activity

New credit, or “credit inquiries,” makes up approximately 10% of your FICO score. This factor looks at how many new credit accounts you’ve recently opened and how many hard inquiries have been made on your credit report. While opening new accounts is a necessary part of credit growth, too many inquiries or new accounts in a short period can be a red flag for lenders.

Hard vs. Soft Inquiries:

- Hard Inquiries: These occur when a lender checks your credit report in response to an application for new credit (e.g., a loan, credit card, or mortgage). Each hard inquiry can slightly lower your score for a short period (typically a few points for up to one year, though they remain on your report for two).

- Soft Inquiries: These occur when you check your own credit report, or when a lender pre-approves you for an offer. Soft inquiries do not affect your credit score.

Why the Concern with New Credit?

Multiple hard inquiries in a short timeframe can signal to lenders that you might be in financial distress and desperately seeking credit, which increases their perceived risk. It can also indicate that you are taking on a lot of new debt, which could strain your ability to make payments.

Strategies for Optimizing New Credit:

- Apply for credit only when needed: Resist the temptation to apply for every credit card offer you receive. Only apply for credit when you genuinely need it.

- Shop for rates wisely: If you’re rate shopping for a mortgage or auto loan, FICO models often treat multiple inquiries for the same type of loan within a specific window (typically 14-45 days, depending on the model) as a single inquiry. This allows you to compare rates without undue penalty.

- Space out applications: If you need multiple new credit lines, try to space out your applications over several months.

Factor 5: Credit Mix – Demonstrating Diverse Financial Management

The final factor, credit mix, accounts for approximately 10% of your FICO score. This element assesses the variety of credit accounts you have. Lenders like to see that you can responsibly manage different types of credit, such as revolving credit (e.g., credit cards) and installment credit (e.g., mortgages, auto loans, student loans).

Understanding Different Credit Types:

- Revolving Credit: These accounts allow you to borrow up to a certain limit, pay it back, and then borrow again. Credit cards and lines of credit are common examples.

- Installment Credit: These loans involve a fixed amount borrowed that is repaid in regular, equal installments over a set period. Mortgages, car loans, and student loans fall into this category.

Why is a Diverse Mix Beneficial?

Having a healthy mix of both revolving and installment credit demonstrates your versatility and ability to handle various financial obligations. It shows lenders that you’re not solely reliant on one type of credit and can manage different payment structures effectively. For instance, successfully managing a credit card (revolving) and an auto loan (installment) simultaneously paints a picture of a well-rounded and responsible borrower.

Strategies for Optimizing Credit Mix:

- Don’t overdo it: While a mix is good, don’t open accounts you don’t need just to diversify. The negative impact of unnecessary debt or hard inquiries will outweigh any benefit from a slightly better mix.

- Natural progression: For most people, a healthy credit mix develops naturally over time. You might start with a credit card, then get an auto loan, and eventually a mortgage. This organic progression is ideal.

- Secured loans: If you’re new to credit or rebuilding, a secured loan or a credit-builder loan can be an effective way to introduce installment credit into your mix responsibly.

Beyond the Big Five: Other Influencing Factors and Nuances

While the five factors discussed above are the primary drivers of your US Credit Score Factors, it’s important to acknowledge that credit scoring is a complex system with many nuances. Here are a few additional considerations:

Credit Report Accuracy:

Your credit score is only as accurate as the information in your credit report. Errors can negatively impact your score. Regularly checking your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) and disputing any inaccuracies is a crucial part of credit management. You are entitled to a free copy of your credit report from each bureau annually through AnnualCreditReport.com.

Authorized Users:

Being an authorized user on someone else’s credit card can impact your score, positively or negatively, depending on how that account is managed. If the primary cardholder has excellent payment history and low utilization, it can help your score. However, if they misuse the card, it could harm your credit.

Credit Building Alternatives:

For those with limited or no credit history, secured credit cards, credit-builder loans, and becoming an authorized user are excellent ways to start establishing a positive credit profile. Some newer models also consider alternative data like rent and utility payments, though these are not universally applied by all lenders or scoring models yet.

The Impact of Time:

Negative information on your credit report, such as late payments or bankruptcies, doesn’t stay there forever. Most negative items fall off after seven years (bankruptcies can remain for 10 years). As time passes, the impact of these derogatory marks diminishes, and a consistent record of positive financial behavior will eventually outweigh past mistakes.

Monitoring Your Score:

Many financial institutions and credit card companies now offer free credit score monitoring services. Utilize these tools to keep an eye on your score and detect any significant changes or potential fraud early on. Understanding the movement of your US Credit Score Factors is key to maintaining financial health.

The Future of Credit Scoring in 2026 and Beyond

As technology advances and financial data becomes more accessible, credit scoring models are continually evolving. While the core five factors are expected to remain paramount in 2026, we may see further integration of alternative data sources. For example, some lenders are already experimenting with using rental payment history, utility payments, and even banking transaction data to assess creditworthiness, particularly for consumers with thin credit files.

The emphasis on financial inclusion and fair lending practices also means that scoring models are constantly being scrutinized and refined to ensure they are equitable and provide accurate assessments across diverse populations. Staying informed about these potential shifts will be beneficial, but focusing on the foundational US Credit Score Factors will always be your most reliable strategy.

Conclusion: Your Action Plan for Credit Success

Mastering your US credit score in 2026 boils down to a clear understanding and consistent application of the knowledge surrounding these five critical factors: payment history, credit utilization, length of credit history, new credit, and credit mix. Each plays a distinct role, but together, they paint a comprehensive picture of your financial behavior.

To recap, here’s your actionable summary:

- Payment History (35%): Always pay your bills on time. Set reminders, automate payments, and communicate with creditors if you foresee issues.

- Credit Utilization (30%): Keep your credit card balances low, ideally below 30% of your available credit, and even lower for optimal scores.

- Length of Credit History (15%): Maintain old accounts in good standing and allow time to build a long, positive credit track record.

- New Credit (10%): Be judicious with new credit applications. Only apply when necessary and space out applications.

- Credit Mix (10%): Responsibly manage a healthy mix of revolving and installment credit as your financial life progresses naturally.

Your credit score is not a static entity; it’s a dynamic reflection of your financial journey. By diligently managing these US Credit Score Factors, you are not just aiming for a higher number; you are actively building a stronger financial foundation that will open doors to better opportunities and greater financial freedom for years to come. Take control of your credit today, and secure a brighter financial tomorrow.