Inflation-Proof Your Portfolio: 2026 Strategies for 3.2% Inflation

Anúncios

Inflation-Proof Your Portfolio: Expert Strategies for a 2026 Economic Climate with 3.2% Inflation (Practical Solutions, Financial Impact)

The specter of inflation is a constant companion in the world of finance, a silent thief that erodes purchasing power and diminishes the real value of your hard-earned investments. As we look towards 2026, economic forecasts suggest a persistent, albeit moderate, inflation rate hovering around 3.2%. While this might not sound alarming at first glance, its cumulative effect can significantly impact your financial future if your portfolio isn’t adequately prepared. This comprehensive guide is designed to equip you with expert strategies to inflation-proof your portfolio, offering practical solutions and a deep dive into the financial impact of such an economic climate.

Understanding the nuances of inflation and its potential effects on various asset classes is the first step towards building a resilient investment strategy. A 3.2% inflation rate means that something costing $100 today will cost approximately $103.20 next year, and this seemingly small increase compounds over time. For investors, this translates into a need for returns that not only cover the nominal growth of their investments but also outpace the rate of inflation to ensure real wealth preservation and growth. The goal is not just to make money, but to ensure that the money you make retains its value and continues to grow in real terms.

Anúncios

In this article, we will delve into the intricacies of inflation, assess its projected impact on the 2026 economy, and, most importantly, provide actionable strategies to safeguard and grow your wealth. We will explore a diverse range of investment vehicles, from traditional assets to alternative investments, evaluating their effectiveness in an inflationary environment. Our focus is on empowering you with the knowledge and tools to make informed decisions, transforming potential challenges into opportunities for robust portfolio performance.

The Landscape of 2026: Understanding 3.2% Inflation and Its Roots

Before we can effectively inflation-proof your portfolio, it’s crucial to understand the underlying factors contributing to the projected 3.2% inflation for 2026. Inflation isn’t a monolithic phenomenon; it’s often a complex interplay of demand-pull, cost-push, and structural factors. Demand-pull inflation occurs when aggregate demand in an economy outstrips aggregate supply, leading to higher prices as consumers compete for limited goods and services. Cost-push inflation, on the other hand, arises from increases in the cost of production, such as rising wages, raw material prices, or energy costs, which businesses then pass on to consumers.

Anúncios

For 2026, several factors could contribute to a sustained 3.2% inflation rate. Supply chain disruptions, while showing signs of easing, could still exert upward pressure on prices in certain sectors. Geopolitical tensions can impact energy prices and commodity markets, leading to cost-push inflation. Furthermore, robust consumer demand, fueled by potentially strong labor markets and accumulated savings, could contribute to demand-pull pressures. Government fiscal policies and central bank monetary policies also play a critical role. While central banks aim for price stability, their actions can sometimes lead to inflationary pressures, either through expansive monetary policies or by failing to tighten policy sufficiently in response to rising prices.

Understanding these drivers is not merely academic; it informs our investment decisions. For instance, if inflation is primarily driven by rising commodity prices, investments in commodity-related assets might be more effective. If it’s a result of strong consumer spending, companies with strong pricing power and consumer staples might be more resilient. The 3.2% projection for 2026 serves as a benchmark, a signal that while extreme hyperinflation might not be on the horizon, ignoring this level of price erosion would be a costly mistake for any investor.

Economists and financial analysts constantly monitor these indicators to refine their forecasts. The 3.2% figure represents a consensus view, suggesting that while the immediate post-pandemic surge in inflation may have receded, a new, more persistent baseline could be establishing itself. This necessitates a proactive approach to portfolio management, moving beyond passive strategies to actively seek out investments that can thrive, or at least maintain their value, in this environment. The goal of inflation proof portfolio management is to ensure that the real return on your investments remains positive, preserving your future purchasing power, which is paramount for long-term financial security.

The Financial Impact: How 3.2% Inflation Affects Your Wealth

A 3.2% inflation rate, sustained over several years, can have a profound impact on your financial well-being, often in ways that are not immediately apparent. It’s not just about the price of goods and services increasing; it’s about the erosion of the real value of your savings, investments, and future income streams. To truly inflation-proof your portfolio, you must first grasp the full scope of this financial impact.

Erosion of Savings and Cash Holdings

Perhaps the most straightforward impact of inflation is on cash and traditional savings accounts. If your cash earns 0.5% interest in a savings account and inflation is 3.2%, your real return is -2.7%. This means that every year, the purchasing power of your savings decreases. Over time, this can significantly diminish the value of your emergency fund or any cash reserves you hold, making it more expensive to achieve future financial goals.

Impact on Fixed-Income Investments

Bonds and other fixed-income investments are particularly vulnerable to inflation. When you invest in a bond, you essentially lend money in exchange for fixed interest payments. If inflation rises above the bond’s yield, the real return on that bond becomes negative. For example, a bond yielding 2% with 3.2% inflation results in a real loss of 1.2% per year. This makes traditional fixed-income strategies less effective for preserving wealth in an inflationary environment, forcing investors to seek alternatives or re-evaluate their bond allocations.

Challenges for Equity Markets

The impact of inflation on equity markets is more nuanced. While some companies can pass on higher costs to consumers, maintaining their profit margins, others may struggle. Companies with strong pricing power, low debt, and essential products or services tend to perform better. Conversely, companies with high operating leverage, thin margins, or those heavily reliant on imported goods may see their profitability squeezed. High inflation can also lead to central banks raising interest rates, which can increase borrowing costs for companies and make future earnings less valuable, potentially dampening stock valuations.

Real Estate and Commodities

Historically, real estate and commodities have been considered good hedges against inflation. Real estate values often rise with inflation, and rental income can be adjusted to keep pace with rising costs. Commodities, by their very nature, are raw materials whose prices often increase during inflationary periods. However, these asset classes are not without their risks and require careful consideration and diversification. A 3.2% inflation rate can be a sweet spot for certain real estate investments, but rising interest rates could also impact mortgage affordability and property demand.

The Hidden Tax of Inflation

Inflation acts as a hidden tax, silently eroding your wealth. It reduces the real value of your future pension payments, makes it more expensive to fund your retirement, and increases the cost of education, healthcare, and other essential services. Without a strategy to inflation-proof your portfolio, your long-term financial goals become increasingly difficult to achieve. The goal is to ensure that your investments are working harder than inflation, providing you with real returns that enhance, rather than diminish, your future purchasing power.

Practical Solutions: Strategies to Inflation-Proof Your Portfolio

Now that we understand the landscape and the potential impact of 3.2% inflation, let’s explore practical strategies to inflation-proof your portfolio. The key is diversification and a thoughtful allocation to assets that have historically performed well during inflationary periods or are designed to offer protection against rising prices.

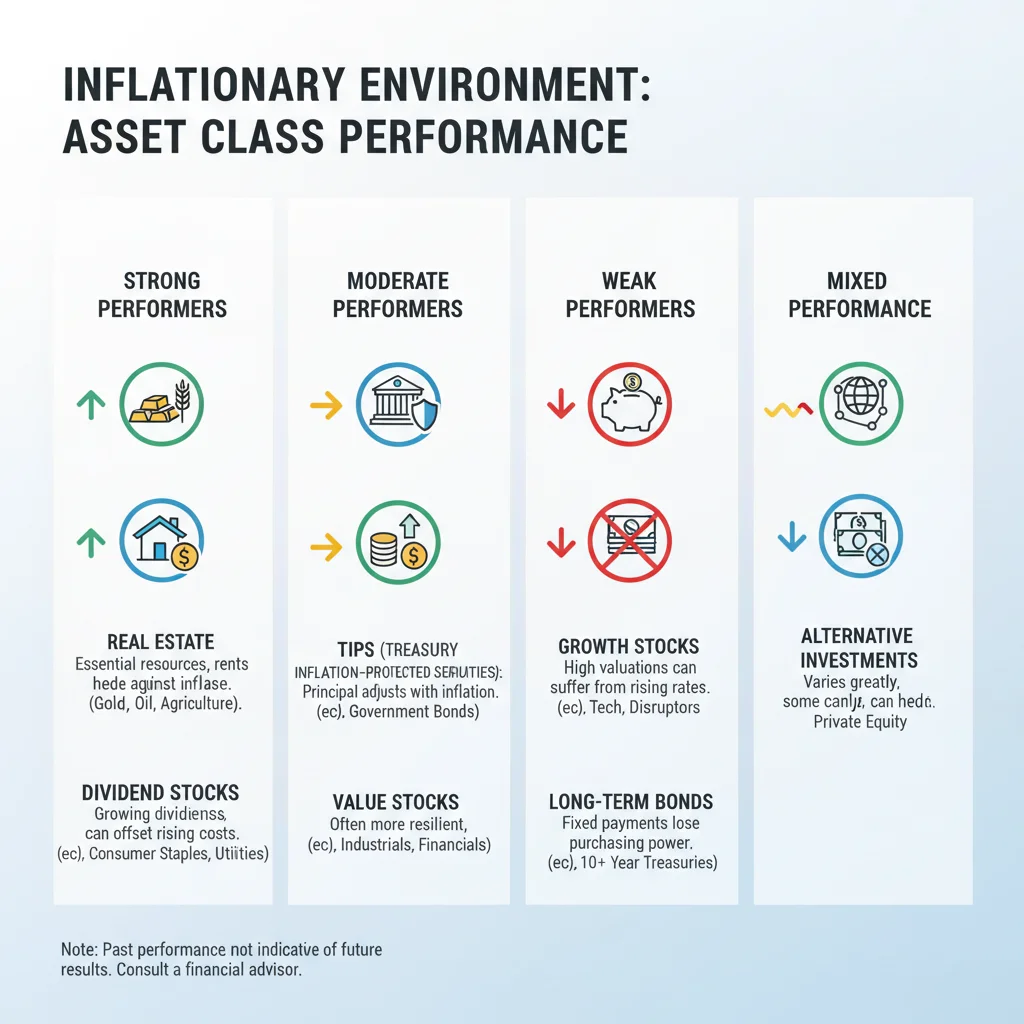

1. Treasury Inflation-Protected Securities (TIPS)

TIPS are government bonds designed to protect investors from inflation. The principal value of a TIPS bond adjusts with the Consumer Price Index (CPI), meaning it rises with inflation and falls with deflation. When the bond matures, you receive either the adjusted principal or the original principal, whichever is greater. You also receive fixed interest payments twice a year, which are applied to the adjusted principal, so your interest payments also increase with inflation. TIPS are one of the most direct ways to hedge against inflation and should be a cornerstone of any inflation-proof portfolio, especially for the fixed-income portion.

2. Real Estate and Real Estate Investment Trusts (REITs)

Real estate has long been considered a strong inflation hedge. Property values and rental income tend to increase with inflation, providing a natural shield against rising prices. Investing directly in physical real estate can be capital-intensive and illiquid. A more accessible option is Real Estate Investment Trusts (REITs). REITs are companies that own, operate, or finance income-producing real estate. They trade on major stock exchanges like stocks, offering liquidity and diversification. REITs often have strong dividend yields and the potential for capital appreciation, making them attractive in an inflationary environment.

3. Commodities and Natural Resources

Commodities, such as oil, gas, precious metals (gold, silver), and agricultural products, often see their prices increase during inflationary periods. This is because they are the raw materials that go into producing goods and services, and their costs are passed on to consumers. Gold, in particular, has a long history as a store of value and an inflation hedge. Investors can gain exposure to commodities through futures contracts, exchange-traded funds (ETFs) that track commodity indices, or by investing in companies involved in commodity production and extraction. Diversifying across various commodities can help mitigate the volatility inherent in individual commodity markets.

4. Value Stocks and Dividend-Paying Stocks

In an inflationary environment, companies with strong balance sheets, consistent earnings, and the ability to pass on rising costs to consumers tend to perform better. These often include value stocks – companies that are undervalued by the market relative to their intrinsic worth. Additionally, dividend-paying stocks, particularly those from established companies with a history of increasing dividends, can provide a growing income stream that helps offset inflation. Look for companies in sectors like consumer staples, utilities, and infrastructure, which tend to be more resilient during economic shifts.

5. Short-Duration Bonds and Floating-Rate Securities

While long-term fixed-rate bonds suffer during inflation, short-duration bonds are less sensitive to interest rate changes. Their shorter maturity means their principal is returned sooner, allowing investors to reinvest at potentially higher rates. Floating-rate securities, whose interest payments adjust periodically based on a benchmark rate, also offer protection as their yields will rise with inflation-driven interest rate hikes. These can be valuable components of the fixed-income portion of an inflation-proof portfolio.

6. International Investments (Selectively)

Diversifying internationally can also play a role, especially if inflation rates vary significantly across different economies. Investing in countries with lower inflation or different economic cycles can provide a hedge. However, this strategy requires careful research into currency risks and the specific economic conditions of each target country. Emerging markets, while carrying higher risk, can sometimes offer higher growth potential that outpaces inflation.

7. Private Equity and Alternative Investments

For accredited investors, private equity and other alternative investments like infrastructure funds can offer inflation protection. These assets are often less correlated with public markets and can benefit from long-term contracts that include inflation escalators. However, they typically come with higher fees, illiquidity, and require significant due diligence.

Implementing Your Inflation-Proof Portfolio Strategy

Building an inflation-proof portfolio isn’t a one-time event; it’s an ongoing process that requires regular review and adjustment. Here’s how to implement these strategies effectively:

Assess Your Current Portfolio

Start by thoroughly reviewing your existing investments. Understand your current asset allocation, identify your exposure to inflation-sensitive assets, and determine where your portfolio might be vulnerable. Use financial planning tools or consult with a financial advisor to get a clear picture of your current standing.

Determine Your Risk Tolerance

Your risk tolerance should always guide your investment decisions. While some inflation hedges, like commodities, can be volatile, others, like TIPS, are more conservative. Tailor your strategy to align with your comfort level for risk, ensuring that your adjustments don’t lead to undue stress or impulsive decisions.

Gradual Adjustments and Diversification

Avoid making drastic, sudden changes to your portfolio. Instead, implement adjustments gradually over time. Diversification remains paramount. Don’t put all your eggs in one inflation-proof basket. A well-diversified portfolio that includes a mix of inflation hedges, growth assets, and defensive positions will be best positioned to navigate various economic scenarios.

Regular Monitoring and Rebalancing

The economic landscape is constantly evolving. Monitor inflation data, economic forecasts, and the performance of your chosen assets regularly. Rebalance your portfolio periodically to ensure it remains aligned with your long-term goals and continues to offer adequate protection against inflation. This might mean trimming positions that have performed exceptionally well and adding to those that are still undervalued or offer better inflation protection.

Consult a Financial Advisor

For many, navigating the complexities of inflation and portfolio management can be challenging. A qualified financial advisor can provide personalized guidance, help you assess your situation, and develop a tailored strategy to inflation-proof your portfolio. They can also help you understand the tax implications of various investment decisions.

Beyond Investment: Personal Finance Strategies for Inflation

While investment strategies are crucial for an inflation-proof portfolio, it’s also important to consider personal finance adjustments that can mitigate the impact of 3.2% inflation on your everyday life. These practical steps can complement your investment efforts and provide a more holistic approach to financial resilience.

Manage Debt Wisely

High-interest debt, such as credit card debt, becomes even more burdensome during inflationary periods, especially if interest rates rise. Prioritize paying down consumer debt to free up cash flow and reduce your exposure to rising interest costs. Consider refinancing fixed-rate debt if current rates are favorable, but be cautious with variable-rate loans.

Review Your Budget and Spending

Inflation means your money buys less. Regularly review your budget to identify areas where you can cut back or optimize spending. Look for opportunities to reduce discretionary expenses, negotiate better deals on services, and make conscious choices about your purchases. This disciplined approach can help maintain your purchasing power.

Increase Your Income

One of the most direct ways to combat inflation is to increase your income. This could involve seeking a raise at your current job, pursuing a promotion, acquiring new skills that command higher wages, or exploring side hustles. A higher income stream provides more capital to invest and helps offset the rising cost of living.

Optimize Your Emergency Fund

While holding too much cash can be detrimental during inflation, an adequate emergency fund is still vital. Consider placing your emergency fund in a high-yield savings account or a short-term certificate of deposit (CD) that offers a slightly better return than a traditional savings account, even if it doesn’t fully beat inflation. The goal is liquidity and some protection, not aggressive growth.

Invest in Yourself

Education, skill development, and career advancement are excellent long-term hedges against inflation. By increasing your earning potential, you enhance your ability to keep pace with rising costs and build greater financial security. Investing in your human capital is often one of the best investments you can make.

Consider Indexed Annuities or I-Bonds

For more conservative investors, certain financial products like indexed annuities (which offer returns tied to market indices while providing principal protection) or U.S. Series I Savings Bonds (I-Bonds, whose interest rates adjust with inflation) can offer an additional layer of inflation protection. These options come with their own set of rules and limitations, so thorough research is essential.

The Long View: Why an Inflation-Proof Portfolio Matters

The conversation about inflation-proofing your portfolio isn’t just about navigating the immediate challenges of 2026; it’s about securing your long-term financial future. A sustained 3.2% inflation rate, if not addressed, can significantly derail your retirement plans, diminish the value of your legacy, and make achieving major financial milestones considerably more difficult.

Think about the compounding effect. Over ten years, 3.2% annual inflation will reduce the purchasing power of $100,000 to approximately $72,500. Over twenty years, it dwindles to around $52,600. These figures underscore the critical importance of proactive investment strategies. Your inflation-proof portfolio is not just a defense mechanism; it’s an offensive strategy to ensure your wealth grows in real terms, allowing you to maintain your desired lifestyle and achieve your financial aspirations.

Moreover, building a resilient portfolio fosters peace of mind. Knowing that your investments are strategically positioned to withstand economic pressures can alleviate stress and allow you to focus on other aspects of your life. It’s about taking control of your financial destiny rather than being a passive observer of economic shifts. The strategies discussed – from TIPS and real estate to commodities and dividend stocks – are not merely theoretical concepts; they are actionable steps that can significantly enhance your financial security.

The economic climate of 2026, with its projected 3.2% inflation, serves as a crucial reminder that vigilance and adaptability are key components of successful investing. By understanding the forces at play, assessing their impact, and implementing practical, diversified strategies, you can transform the challenge of inflation into an opportunity for robust portfolio growth and sustained wealth creation. The time to inflation-proof your portfolio is now, ensuring that your financial future remains bright and secure.

Conclusion: Building a Resilient Future in an Inflationary World

As we navigate towards 2026 and beyond, the reality of a persistent 3.2% inflation rate demands a sophisticated and proactive approach to investment management. The days of assuming modest inflation and relying solely on traditional asset allocations are behind us. To truly inflation-proof your portfolio, you must embrace a strategy that is diversified, dynamic, and keenly aware of the specific assets that thrive when prices are on the rise.

We have explored a range of expert strategies, from the direct protection offered by Treasury Inflation-Protected Securities (TIPS) to the tangible value of real estate and commodities. We delved into the resilience of value and dividend-paying stocks, and the strategic advantages of short-duration bonds and floating-rate securities. Beyond investments, we also touched upon essential personal finance adjustments – managing debt, optimizing budgets, and increasing income – all contributing to a comprehensive defense against the erosion of purchasing power.

The financial impact of 3.2% inflation, while seemingly moderate, is significant over time. It affects everything from your everyday spending to your long-term retirement goals. Ignoring it is not an option for those committed to financial well-being. Instead, by carefully assessing your current portfolio, understanding your risk tolerance, and making gradual, informed adjustments, you can build a portfolio that not only withstands inflationary pressures but potentially benefits from them.

Remember, the goal is not just to maintain your nominal wealth, but to preserve and grow your real purchasing power. This requires diligent monitoring, periodic rebalancing, and a willingness to adapt your strategy as economic conditions evolve. Whether you choose to implement these strategies independently or seek the guidance of a qualified financial advisor, the effort to inflation-proof your portfolio is an investment in your future security and prosperity.

Embrace the challenge, apply these practical solutions, and confidently build a resilient portfolio ready to thrive in the 2026 economic climate and beyond. Your financial future depends on it.