Retirement Investing 2026: Ultimate US Guide to Target-Date Funds

Anúncios

The dawn of a new year often brings with it a renewed focus on financial planning, and as we approach 2026, the landscape of retirement investing continues to evolve. For those in the United States looking to secure their golden years, understanding the myriad of investment vehicles and strategies available is paramount. This comprehensive guide delves into the essentials of Retirement Investing 2026, with a particular emphasis on the role of target-date funds, while also exploring other crucial avenues like IRAs, 401ks, and advanced investment approaches. Whether you’re just starting your career or nearing retirement, the insights provided here will help you navigate the complexities and build a robust financial future.

Anúncios

The Imperative of Early Retirement Investing 2026 Planning

Time is arguably your most valuable asset when it comes to Retirement Investing 2026. The magic of compound interest, where your earnings generate their own earnings, works best over extended periods. Starting early, even with modest contributions, can lead to substantial wealth accumulation by the time you reach retirement age. Many people often delay their retirement planning, believing they have ample time, only to find themselves playing catch-up later in life. In 2026, with market dynamics constantly shifting and life expectancies on the rise, proactive and informed planning is more critical than ever.

Beyond the power of compounding, early planning also offers the benefit of flexibility. Life rarely follows a straight path, and unexpected expenses, career changes, or family obligations can sometimes derail even the best-laid financial plans. By starting early, you create a buffer, allowing you to absorb these shocks without completely derailing your retirement goals. It provides the peace of mind that comes from knowing you have a solid foundation in place, even if adjustments become necessary along the way. This foresight is a cornerstone of effective Retirement Investing 2026.

Understanding Your Retirement Goals for 2026

Before diving into specific investment vehicles, it’s crucial to define what retirement means to you. Do you envision a life of extensive travel, pursuing new hobbies, or simply enjoying quiet time at home? Your vision of retirement will directly influence the amount of money you’ll need to save and the investment strategies you should employ. Consider factors like your desired lifestyle, potential healthcare costs, and whether you plan to leave an inheritance. These personal considerations form the bedrock of your Retirement Investing 2026 strategy.

Anúncios

One effective way to clarify your goals is to create a detailed budget for your anticipated retirement lifestyle. This isn’t just about estimating your monthly expenses; it’s about envisioning your day-to-day life and putting a price tag on it. Will you still have a mortgage? What about property taxes, insurance, and utilities? How much will you spend on food, entertainment, and transportation? Don’t forget to factor in potential inflation, which can significantly erode the purchasing power of your savings over time. A clear picture of your future expenses will provide a tangible target for your Retirement Investing 2026 efforts.

The Role of Inflation and Healthcare in Retirement Planning

Inflation is a silent wealth killer. What seems like a comfortable sum today might be insufficient in 20 or 30 years due to the rising cost of living. When planning for Retirement Investing 2026, it’s essential to factor in an average inflation rate (historically around 3% in the US) to ensure your savings maintain their purchasing power. Similarly, healthcare costs are a significant concern for retirees. Medicare covers a portion of expenses, but out-of-pocket costs, prescription drugs, and long-term care can quickly deplete savings. Researching potential healthcare expenses and considering options like long-term care insurance should be an integral part of your retirement financial model.

Exploring Key Retirement Investment Vehicles for 2026

The US offers a robust ecosystem of retirement savings plans, each with its own advantages and disadvantages. Understanding these options is the first step towards building a diversified and resilient Retirement Investing 2026 portfolio.

401(k) Plans: Employer-Sponsored Powerhouses

For many Americans, the 401(k) is the cornerstone of their retirement savings. Offered by employers, these plans allow you to contribute a portion of your pre-tax paycheck, reducing your taxable income in the present. The money grows tax-deferred until retirement, at which point withdrawals are taxed as ordinary income. A significant benefit of 401(k)s is employer matching contributions. If your employer offers a match, it’s essentially free money – a 100% return on your investment right off the bat. Failing to contribute enough to maximize your employer match is one of the biggest mistakes you can make in Retirement Investing 2026.

Beyond the traditional 401(k), some employers also offer Roth 401(k)s. With a Roth 401(k), your contributions are made with after-tax dollars, meaning your qualified withdrawals in retirement are completely tax-free. This can be a powerful advantage, especially if you anticipate being in a higher tax bracket during retirement than you are now. The decision between a traditional and Roth 401(k) often depends on your current income, your expected future income, and your overall tax strategy. For Retirement Investing 2026, it’s wise to consult with a financial advisor to determine which option best suits your individual circumstances.

Individual Retirement Accounts (IRAs): Personal Control and Flexibility

IRAs offer another powerful avenue for Retirement Investing 2026, providing flexibility and control, especially for those whose employers don’t offer a 401(k) or who wish to supplement their employer-sponsored plans.

- Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred. Withdrawals in retirement are taxed as ordinary income. Contribution limits are set annually by the IRS.

- Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free. This is ideal for those who expect to be in a higher tax bracket in retirement. There are income limitations for contributing directly to a Roth IRA.

The choice between a Traditional and Roth IRA, much like with 401(k)s, hinges on your current and projected future tax situation. For many, a combination of both a 401(k) and an IRA provides a well-rounded approach to Retirement Investing 2026, allowing for both tax-deferred and tax-free growth.

Health Savings Accounts (HSAs): The Triple-Tax Advantage

Often overlooked, Health Savings Accounts (HSAs) are a powerful tool for Retirement Investing 2026, especially for those enrolled in a high-deductible health plan (HDHP). HSAs offer a unique triple-tax advantage:

- Contributions are tax-deductible.

- Earnings grow tax-free.

- Qualified withdrawals for medical expenses are tax-free.

If you manage to keep your medical expenses low, you can invest the funds in your HSA, allowing them to grow over time. In retirement, these funds can be used for medical expenses tax-free, or for any purpose after age 65 (though non-medical withdrawals will be taxed as ordinary income, similar to a traditional IRA). Given the escalating cost of healthcare, an HSA can be an invaluable asset in your Retirement Investing 2026 strategy.

Target-Date Funds: A Simplified Approach to Retirement Investing 2026

For many investors, especially those who prefer a hands-off approach, target-date funds have become an incredibly popular option for Retirement Investing 2026. These funds are designed to simplify the investment process by automatically adjusting their asset allocation over time, becoming more conservative as you approach your target retirement date.

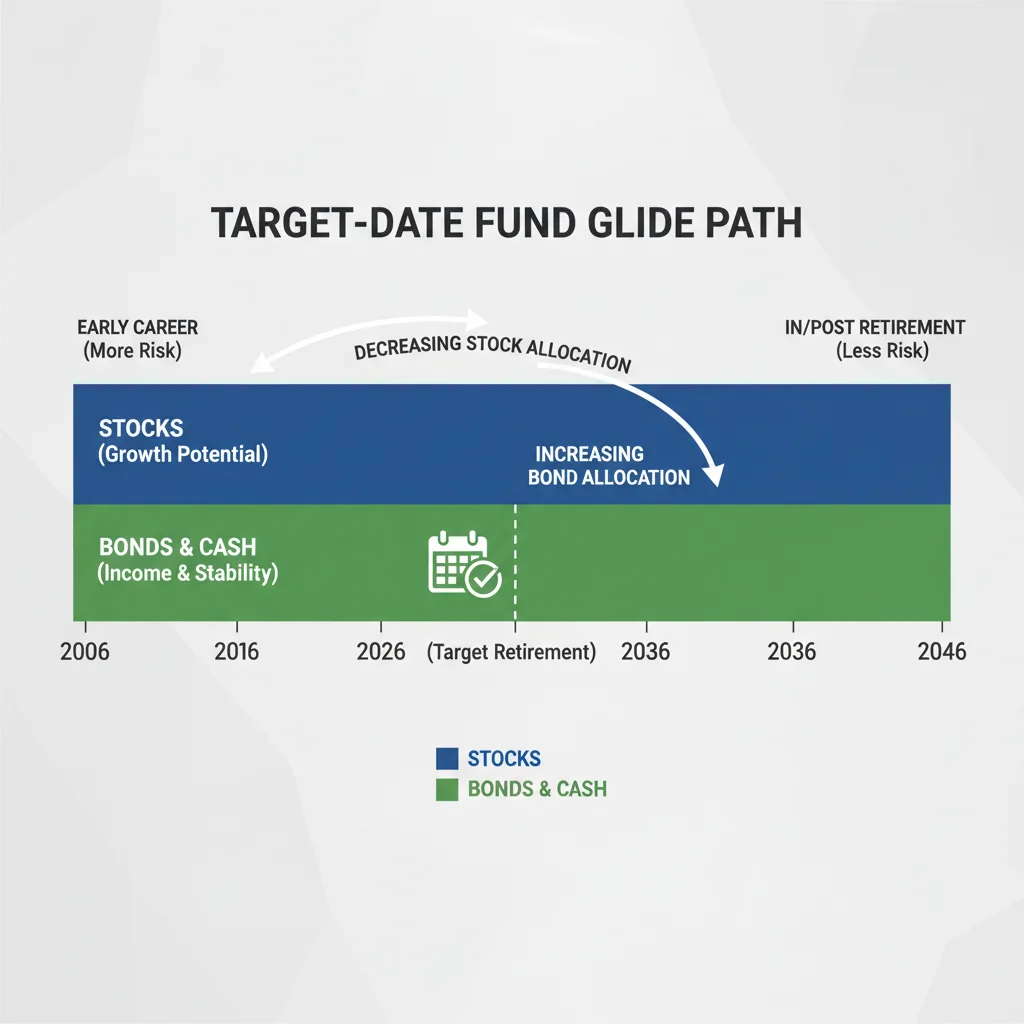

How Target-Date Funds Work

A target-date fund is typically named after a specific year, such as a ‘2025 Target-Date Fund’ or a ‘2060 Target-Date Fund’. When you invest in one of these funds, you select the fund closest to your intended retirement year. The fund’s managers then construct a diversified portfolio that initially holds a higher percentage of growth-oriented assets like stocks. As the target date approaches, the fund’s asset allocation automatically shifts towards more conservative investments, such as bonds and cash equivalents.

This automated rebalancing, often referred to as a ‘glide path’, is the core benefit of target-date funds. It removes the guesswork and emotional decision-making from adjusting your portfolio, ensuring your investments align with your declining risk tolerance as retirement nears. This makes them an excellent choice for Retirement Investing 2026 for those who want a streamlined approach.

Advantages of Target-Date Funds for Retirement Investing 2026

- Simplicity: They offer a set-it-and-forget-it solution, ideal for busy investors or those new to investing.

- Diversification: Each fund typically holds a diversified mix of stocks, bonds, and other assets, spreading risk.

- Automatic Rebalancing: The fund automatically adjusts its risk level over time, aligning with your changing needs.

- Professional Management: Experienced fund managers make the investment decisions.

Potential Downsides and Considerations

While target-date funds offer significant advantages for Retirement Investing 2026, they also have some potential drawbacks:

- Fees: Like all mutual funds, target-date funds charge management fees, which can vary significantly. Be sure to compare expense ratios.

- Generic Glide Path: The glide path is designed for a broad average investor. It might not perfectly align with your individual risk tolerance or financial situation.

- Lack of Customization: You give up some control over individual asset allocation decisions.

- Fund Performance: Performance can vary widely between different target-date fund providers. Research the underlying investments and historical returns.

When selecting a target-date fund for your Retirement Investing 2026, pay close attention to the expense ratio, the specific glide path (how quickly they shift from aggressive to conservative), and the underlying investments. A lower expense ratio can save you thousands of dollars over the long term, and understanding the glide path ensures it aligns with your personal comfort level regarding risk.

Advanced Strategies for Retirement Investing 2026

Beyond the fundamental options, savvy investors might consider more advanced strategies to optimize their Retirement Investing 2026 portfolio. These often require a deeper understanding of market dynamics and a higher comfort level with risk.

Diversification Beyond Target-Date Funds

While target-date funds offer inherent diversification, some investors prefer to build their own diversified portfolio using a mix of individual stocks, bonds, exchange-traded funds (ETFs), and mutual funds. This approach allows for greater customization and potentially lower fees if you choose low-cost index funds or ETFs. A well-diversified portfolio should include:

- US Equities: Large-cap, mid-cap, and small-cap stocks.

- International Equities: Developed and emerging markets.

- Bonds: Government bonds, corporate bonds, and high-yield bonds.

- Alternative Investments: Real estate, commodities, or even cryptocurrencies (with caution and a small allocation).

The key to successful diversification in Retirement Investing 2026 is ensuring that different asset classes respond differently to market conditions, thus reducing overall portfolio volatility.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy that involves selling investments at a loss to offset capital gains and potentially a limited amount of ordinary income. While it doesn’t directly increase your investment returns, it can reduce your tax liability, effectively boosting your net gains. This strategy is particularly useful in taxable brokerage accounts, rather than tax-advantaged accounts like 401(k)s or IRAs, where gains and losses aren’t taxed annually. Implementing tax-loss harvesting requires careful planning and adherence to IRS rules, such as the wash-sale rule, but it can be a valuable tool for optimizing your Retirement Investing 2026.

Rebalancing Your Portfolio

Even if you don’t use a target-date fund, regular rebalancing is crucial. Over time, market fluctuations can cause your asset allocation to drift from your target. For example, a strong stock market might lead to stocks making up a larger percentage of your portfolio than intended, increasing your risk exposure. Rebalancing involves selling off some of your overperforming assets and buying more of your underperforming ones to bring your portfolio back to your desired allocation. This disciplined approach helps maintain your risk profile and is a vital component of successful Retirement Investing 2026.

Considering Annuities for Income Certainty

As you approach retirement, annuities can play a role in providing a guaranteed income stream, addressing a key concern for many retirees: outliving their savings. An annuity is a contract between you and an insurance company where you make payments, and in return, the insurer promises to make regular payments to you, either immediately or at some point in the future. There are various types of annuities, including fixed, variable, and indexed, each with different risk and return profiles.

While annuities offer income certainty, they can also come with high fees and complex terms. It’s essential to understand the surrender charges, riders, and payout options before committing to an annuity. For some, a portion of their Retirement Investing 2026 portfolio allocated to an annuity can provide peace of mind, but it’s crucial to weigh the benefits against the costs and complexities.

Key Considerations for Retirement Investing 2026

As you build and manage your retirement portfolio, several overarching principles should guide your decisions.

Risk Tolerance and Time Horizon

Your risk tolerance – how comfortable you are with the potential for your investments to lose value – should be a primary driver of your investment choices. Coupled with your time horizon (how long until you need the money), these two factors dictate your appropriate asset allocation. Younger investors with a longer time horizon can typically afford to take on more risk, investing a higher percentage in stocks, which offer greater growth potential. As retirement approaches, a more conservative approach with a higher allocation to bonds is generally recommended to preserve capital. For Retirement Investing 2026, understanding your personal risk profile is non-negotiable.

Fees and Expenses

Even seemingly small fees can significantly erode your retirement savings over decades. Pay close attention to expense ratios for mutual funds and ETFs, advisory fees, and transaction costs. Opting for low-cost index funds or ETFs can save you hundreds of thousands of dollars over your investing lifetime. When comparing investment options for Retirement Investing 2026, always scrutinize the fee structure.

Staying Informed and Adapting

The financial world is dynamic. Economic conditions, market trends, and tax laws can change. While a ‘set-it-and-forget-it’ approach can work for some aspects, it’s crucial to stay informed about broader economic shifts and review your retirement plan periodically. This doesn’t mean constantly tinkering with your portfolio, but rather conducting an annual check-up to ensure your investments are still aligned with your goals and risk tolerance. Regular reviews are a hallmark of effective Retirement Investing 2026.

Common Pitfalls to Avoid in Retirement Investing 2026

Even with the best intentions, investors can fall prey to common mistakes that derail their retirement plans. Being aware of these pitfalls can help you avoid them.

Emotional Investing

Reacting emotionally to market fluctuations is a leading cause of poor investment decisions. Selling during a market downturn out of fear, or buying into a hot stock purely based on hype, rarely leads to long-term success. A disciplined, long-term approach, sticking to your predetermined investment strategy, is far more effective. For Retirement Investing 2026, patience and discipline are virtues.

Not Saving Enough

This might seem obvious, but many people underestimate how much they’ll need in retirement. The ‘Rule of Thumb’ often suggests saving 10-15% of your income, but this can vary significantly based on your desired retirement lifestyle and when you start saving. Use retirement calculators and consider consulting a financial advisor to get a more accurate estimate of your savings needs for Retirement Investing 2026.

Ignoring Inflation

As mentioned earlier, inflation erodes purchasing power. A common mistake is to save a fixed dollar amount without considering how much that money will actually buy in the future. Your investment returns need to outpace inflation to truly grow your wealth. This is a critical factor in successful Retirement Investing 2026.

Failing to Diversify

Putting all your eggs in one basket is a risky strategy. While a single investment might perform exceptionally well, it also carries the risk of significant losses. Diversification across different asset classes, industries, and geographies helps mitigate this risk. Even within target-date funds, it’s worth understanding the underlying diversification.

Cashing Out Retirement Accounts Early

Withdrawing from a 401(k) or IRA before retirement age (typically 59½) can trigger not only income taxes but also a 10% early withdrawal penalty. While there are exceptions, cashing out early should be a last resort, as it significantly hampers your ability to compound wealth for your Retirement Investing 2026 goals.

Seeking Professional Guidance for Retirement Investing 2026

While this guide provides a wealth of information, personal financial situations are unique. A qualified financial advisor can offer personalized advice tailored to your specific goals, risk tolerance, and time horizon. They can help you:

- Develop a comprehensive retirement plan.

- Select appropriate investment vehicles.

- Optimize your tax strategy.

- Navigate complex financial decisions.

- Stay disciplined through market ups and downs.

When choosing an advisor for your Retirement Investing 2026, look for a Certified Financial Planner (CFP) who acts as a fiduciary, meaning they are legally obligated to act in your best interest. This can provide an invaluable layer of expertise and accountability.

The Future of Retirement Investing Beyond 2026

The financial landscape is constantly evolving. Technological advancements, global economic shifts, and changes in regulatory frameworks will continue to shape how we approach retirement planning. Keeping an eye on these trends is crucial for long-term success in Retirement Investing 2026 and beyond.

Technological Innovations

Robo-advisors, powered by algorithms, are making investing more accessible and affordable. These platforms can manage diversified portfolios, rebalance automatically, and even implement tax-loss harvesting strategies with minimal human intervention. While they may not offer the personalized touch of a human advisor, they are an excellent option for cost-conscious investors or those with simpler financial needs.

ESG Investing

Environmental, Social, and Governance (ESG) investing is gaining traction, allowing investors to align their portfolios with their values. Many fund providers now offer ESG-focused ETFs and mutual funds. As awareness grows, integrating ESG factors into your Retirement Investing 2026 strategy could become a more prominent consideration.

Longevity and Healthcare Advancements

As people live longer, the need for a more substantial retirement nest egg becomes even more pronounced. Advances in healthcare could also lead to new treatments and therapies, but potentially at a higher cost. These factors underscore the importance of robust savings and flexible planning for Retirement Investing 2026 and the decades that follow.

Conclusion: Your Path to a Secure Retirement in 2026 and Beyond

Securing your financial future for retirement is a journey, not a destination. It requires consistent effort, informed decision-making, and a willingness to adapt. By understanding the core principles of Retirement Investing 2026, leveraging powerful tools like target-date funds, 401(k)s, and IRAs, and avoiding common pitfalls, you can build a robust portfolio that supports your desired lifestyle in your golden years.

Start early, define your goals, diversify wisely, manage fees, and don’t hesitate to seek professional guidance. The financial decisions you make today will profoundly impact your tomorrow. Take control of your Retirement Investing 2026 now, and look forward to a future filled with financial security and peace of mind.