Roth IRA Conversions: 2026 Tax Planning for US Savers

The Latest on Roth IRA Conversions: What US Savers Need to Know for 2026 Tax Planning

Anúncios

As US savers navigate the ever-evolving landscape of retirement planning, the concept of a Roth IRA Conversion continues to be a powerful strategy. With an eye towards 2026, understanding the nuances of these conversions is more critical than ever. This comprehensive guide delves into the latest considerations, strategies, and potential pitfalls associated with Roth IRA conversions, helping you make informed decisions for your financial future.

The allure of tax-free withdrawals in retirement makes the Roth IRA an incredibly attractive vehicle. However, not everyone qualifies for direct contributions, which is where the Roth IRA Conversion comes into play. By converting traditional IRA, 401(k), or other pre-tax retirement funds into a Roth account, you pay taxes on the converted amount upfront, in exchange for tax-free growth and distributions later on. This strategy is particularly potent when current tax rates are perceived to be lower than future tax rates, a scenario many financial experts are contemplating as 2026 approaches.

Anúncios

Understanding the Basics of a Roth IRA Conversion

Before diving into advanced strategies for 2026, let’s establish a solid understanding of what a Roth IRA Conversion entails. Essentially, it’s the process of moving money from a traditional (pre-tax) retirement account into a Roth (post-tax) retirement account. The key implication of this move is that any funds converted are subject to income tax in the year of conversion. Once the funds are in the Roth IRA, all qualified distributions in retirement are tax-free.

Who Benefits Most from a Roth IRA Conversion?

A Roth IRA Conversion isn’t a one-size-fits-all solution. It’s most beneficial for individuals who:

- Expect to be in a higher tax bracket in retirement: If you believe your income, and thus your tax bracket, will be higher in your retirement years than it is today, paying taxes now at a lower rate makes significant financial sense.

- Are currently in a low tax bracket: This could be due to a temporary dip in income, early career stages, or significant deductions in a particular year. Seizing these opportunities for a conversion can be highly advantageous.

- Want to leave a tax-free inheritance: Roth IRAs offer a fantastic estate planning tool. Heirs can inherit the Roth IRA tax-free, and they are generally subject to fewer rules regarding required minimum distributions (RMDs) compared to inherited traditional IRAs.

- Don’t need the money in the short term: To fully realize the benefits of a Roth IRA, you need to allow the converted funds to grow for at least five years before making tax-free withdrawals.

- Are not eligible for direct Roth IRA contributions due to high income: For high-income earners who exceed the IRS’s income limitations for direct Roth IRA contributions, a backdoor Roth IRA conversion (converting non-deductible traditional IRA contributions to Roth) is a common strategy.

The Tax Implications of Conversion

The primary tax implication of a Roth IRA Conversion is that the amount converted from a pre-tax account is added to your gross income for the year of conversion. This means you will owe income tax on that amount. It’s crucial to factor this into your financial planning for the conversion year. For instance, if you convert $50,000 from a traditional IRA and are in a 24% tax bracket, you would owe an additional $12,000 in taxes that year.

Anúncios

It’s generally recommended to pay the taxes due on the conversion from funds outside of your retirement accounts. If you use funds from the IRA itself to pay the tax, those funds are considered an early withdrawal and may be subject to an additional 10% penalty if you are under 59½ years old.

Why 2026 is a Crucial Year for Roth IRA Conversion Planning

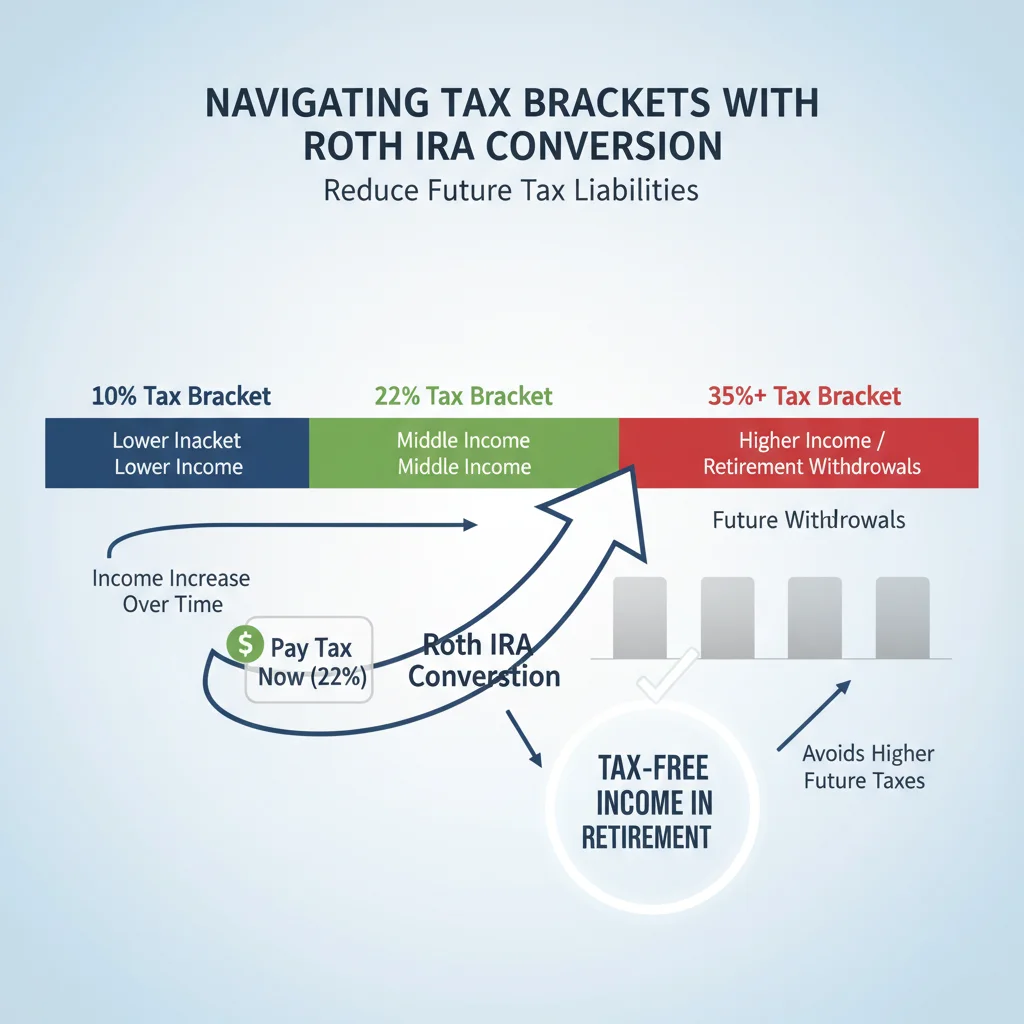

The year 2026 holds particular significance for Roth IRA Conversion planning due to the scheduled expiration of certain provisions from the Tax Cuts and Jobs Act (TCJA) of 2017. Many of the individual income tax rate reductions enacted by the TCJA are set to expire at the end of 2025. This means that, absent new legislation, tax rates are projected to revert to higher levels starting in 2026.

Anticipated Tax Rate Changes

If the TCJA provisions expire as scheduled, many taxpayers could find themselves in higher marginal tax brackets in 2026 and beyond. This creates a compelling window of opportunity in 2024 and 2025 to perform a Roth IRA Conversion while tax rates are potentially lower. Paying taxes now at a 24% or 32% rate might be preferable to paying them at a 28% or 35% rate in the future, especially considering the compounding growth of tax-free funds within a Roth IRA.

Savvy investors are already looking ahead, modeling different tax scenarios to determine the optimal timing and amount for their conversions. This forward-looking approach is central to effective retirement planning.

Strategic Timing and Tax Bracket Management

Considering the potential tax rate increases in 2026, many financial advisors are recommending that clients consider a series of smaller Roth IRA conversions over the next few years, rather than one large conversion. This strategy, often referred to as ‘tax bracket management,’ allows you to convert amounts that keep you within your current tax bracket or prevent you from jumping into a significantly higher one.

For example, instead of converting $100,000 in one year and potentially pushing a large portion of that into a higher tax bracket, you might convert $30,000 each year for three years. This approach can minimize the immediate tax bite while still achieving the long-term benefit of a Roth IRA Conversion.

Strategies for Optimizing Your Roth IRA Conversion

Executing a successful Roth IRA Conversion requires careful planning and consideration of various factors. Here are some key strategies to optimize your conversion process:

1. The Backdoor Roth IRA Strategy

For high-income earners who exceed the income limits for direct Roth IRA contributions, the ‘backdoor Roth’ is a popular and legitimate strategy. This involves contributing non-deductible after-tax money to a traditional IRA, and then immediately converting those funds to a Roth IRA. Since the original contributions were made with after-tax dollars, only any earnings on those contributions would be taxable upon conversion.

It’s crucial to understand the ‘pro-rata’ rule when implementing a backdoor Roth. If you have existing pre-tax traditional IRA money, the conversion will be treated as a pro-rata mix of your pre-tax and after-tax IRA funds, meaning a portion of the conversion will be taxable. To avoid this, some individuals consider converting all existing pre-tax IRA money to a Roth IRA before executing the backdoor strategy, or rolling pre-tax IRA funds into an employer-sponsored plan like a 401(k), if permitted.

2. The ‘Roth Ladder’ Strategy

The Roth Ladder is a strategy often employed by those planning for early retirement or who need access to their Roth funds before age 59½. While direct contributions to a Roth IRA can be withdrawn tax- and penalty-free at any time, converted amounts are subject to a five-year waiting period for tax- and penalty-free withdrawals. If you withdraw converted funds within five years of the conversion, the portion representing the original conversion amount (not earnings) may be subject to a 10% early withdrawal penalty.

With a Roth Ladder, you perform a series of conversions over several years. Each conversion has its own five-year clock. By staggering your conversions, you create a ‘ladder’ of funds that become accessible tax- and penalty-free at different points, providing liquidity in early retirement without incurring penalties.

3. Consider a ‘Partial’ Roth IRA Conversion

You don’t have to convert your entire traditional IRA balance at once. A partial Roth IRA Conversion allows you to convert only a portion of your funds, helping you manage the associated tax liability. This is particularly useful for managing your tax bracket, as discussed earlier. By converting smaller amounts each year, you can stay within a desirable tax bracket and avoid a significant tax shock in any single year.

4. The Role of Net Unrealized Appreciation (NUA)

For those with employer-sponsored plans (like a 401(k)) that hold company stock, the Net Unrealized Appreciation (NUA) rule can be a powerful consideration alongside a Roth IRA Conversion. When you leave an employer, you can often roll your 401(k) into an IRA. However, if your 401(k) contains company stock that has appreciated significantly, you might consider distributing the company stock to a taxable brokerage account and rolling the rest of your 401(k) into an IRA.

The NUA strategy allows you to pay ordinary income tax only on the cost basis of the company stock in the year of distribution. The appreciation (NUA) is then taxed at long-term capital gains rates when you eventually sell the stock, which are typically lower than ordinary income tax rates. This can be combined with a Roth IRA conversion strategy for the non-company stock portion of your 401(k).

Potential Pitfalls and How to Avoid Them

While the benefits of a Roth IRA Conversion are substantial, there are several potential pitfalls that savers must be aware of to ensure the strategy is executed effectively.

1. Underestimating the Tax Liability

The most common mistake is failing to adequately plan for the tax bill that comes with a conversion. Remember, the converted amount is added to your taxable income. This can push you into a higher tax bracket, increase your Medicare premiums (IRMAA), and even affect the taxation of your Social Security benefits. Always consult with a tax professional to understand the full impact of a conversion on your overall tax picture.

2. Not Having Funds to Pay the Tax

As mentioned, it’s best to pay the conversion taxes from non-retirement funds. If you use money from the IRA itself, that portion is considered a distribution and could be subject to early withdrawal penalties if you’re under 59½, in addition to the income tax. This defeats part of the purpose of the conversion.

3. The Five-Year Rule

Each Roth IRA Conversion has its own five-year clock. If you withdraw converted amounts before five years have passed (or before age 59½), you may incur a 10% early withdrawal penalty on the converted principal. Understanding and respecting this rule is vital, especially for those considering early retirement.

4. The Pro-Rata Rule for Backdoor Roth Conversions

If you have existing pre-tax IRA money (from deductible contributions or rollovers from a 401(k)), the pro-rata rule comes into play when performing a backdoor Roth. This rule states that a conversion is treated as coming proportionally from both your pre-tax and after-tax IRA funds. This can make a seemingly tax-free backdoor conversion partially taxable. Consolidating pre-tax IRA accounts into an employer 401(k) before a backdoor conversion can help avoid this.

5. Missing the Recharacterization Deadline (No Longer Applicable)

It’s important to note that the option to ‘recharacterize’ a Roth conversion (undo it) was eliminated by the TCJA for conversions made after December 31, 2017. This means that once you convert, the decision is generally permanent. This makes careful planning even more critical.

The Role of Professional Advice in Roth IRA Conversions

Given the complexities and significant tax implications of a Roth IRA Conversion, seeking professional guidance is highly recommended. A qualified financial advisor and a tax professional can help you:

- Assess your personal financial situation: They can analyze your income, current and projected tax brackets, retirement goals, and overall financial health to determine if a conversion is right for you.

- Model different scenarios: Using specialized software, they can project the long-term benefits and costs of various conversion strategies, including partial conversions over several years.

- Navigate tax rules and regulations: Tax laws are complex and constantly changing. Professionals stay abreast of the latest rules and can ensure your conversion is executed correctly and compliantly.

- Integrate with your broader financial plan: A Roth conversion shouldn’t happen in a vacuum. It should be part of a holistic financial and estate plan.

Don’t underestimate the value of expert advice. The cost of a few hours with a professional can be far less than the potential tax penalties or missed opportunities resulting from an improperly executed conversion.

Case Studies: Illustrating Roth IRA Conversion Strategies

To further illustrate the practical application of a Roth IRA Conversion, let’s consider a couple of hypothetical scenarios:

Case Study 1: The Mid-Career Professional

Sarah, 45, is a successful professional earning $150,000 annually. She has $200,000 in a traditional IRA from a previous employer. She anticipates her income will continue to grow, and she expects to be in a higher tax bracket in retirement. Her current marginal tax rate is 24%.

Sarah’s financial advisor suggests a partial Roth IRA conversion strategy over the next few years, especially before 2026. In 2024 and 2025, while tax rates are potentially lower, she converts $30,000 each year. This adds $30,000 to her income, but keeps her within the 24% tax bracket for most of the converted amount, costing her an additional $7,200 in taxes each year. By 2026, she will have converted $60,000, which will now grow tax-free. Her remaining $140,000 in the traditional IRA can be converted later if tax rates remain favorable, or she can leave it as is.

Benefit: Sarah leverages current potentially lower tax rates to move a significant portion of her retirement savings into a tax-free vehicle, avoiding higher taxes in a future expected higher tax bracket.

Case Study 2: The Early Retiree

Mark, 58, plans to retire at 60. He has a substantial traditional IRA balance of $500,000. He expects his income to drop significantly in his early retirement years (ages 60-65) before he starts collecting Social Security and other pension income. He is currently in the 22% tax bracket.

Mark’s advisor recommends a Roth Ladder strategy. From age 58 to 60, while still working but anticipating lower income years, he converts $50,000 annually. The taxes are paid from his savings. After he retires at 60, his income drops, placing him in a very low tax bracket (e.g., 12%). He continues to convert $50,000 annually for the next few years. The first $50,000 converted at age 58 will be available tax- and penalty-free at age 63 (after the five-year rule and he’s over 59½). Each subsequent conversion creates a new rung on the ladder, providing him with tax-free income streams during his early retirement years when he needs to bridge the gap before other income sources kick in.

Benefit: Mark strategically uses his lower-income years to convert large sums at low tax rates, creating a significant pool of tax-free funds for his early retirement, avoiding penalties and managing his income effectively.

The Future of Roth IRA Conversions Beyond 2026

While 2026 is a significant milestone due to the TCJA expirations, the landscape of retirement planning is always evolving. Future legislation, economic conditions, and individual circumstances will continue to influence the attractiveness and strategy behind a Roth IRA Conversion.

It’s important for savers to remain flexible and regularly review their financial plans. What makes sense today might need adjustments in a few years. Staying informed about potential legislative changes and economic forecasts is key to maintaining an optimized retirement strategy.

The Role of Inflation

Inflation can also play a role in the decision to convert. If you anticipate high inflation in the future, the value of your tax payments today (in current dollars) might be less than the value of future tax payments (in inflated dollars). This can make paying taxes now on a conversion more appealing, as you’re effectively paying with ‘cheaper’ dollars.

Required Minimum Distributions (RMDs)

A significant advantage of Roth IRAs is that they are not subject to Required Minimum Distributions (RMDs) during the original owner’s lifetime. This means your money can continue to grow tax-free for as long as you live, offering greater flexibility in your retirement income planning and significant estate planning benefits. Converting to a Roth IRA can help reduce future RMDs from traditional IRAs, which can be a strategic move to manage future taxable income in retirement.

Conclusion: Proactive Planning for Your Roth IRA Conversion

The Roth IRA Conversion remains one of the most powerful tools in a US saver’s retirement planning arsenal. With 2026 on the horizon and the potential for higher tax rates, the window of opportunity to convert at potentially lower rates is a significant consideration. By understanding the mechanics, strategizing effectively, and avoiding common pitfalls, you can leverage a Roth IRA conversion to build a more tax-efficient and secure financial future.

Remember, this is not a decision to be taken lightly or in isolation. It requires careful analysis of your personal circumstances, a thorough understanding of tax implications, and ideally, the guidance of experienced financial and tax professionals. Start your planning now, look ahead to 2026, and empower your retirement savings with the strategic advantage of a Roth IRA conversion.

2026: Contribution Limits & Smart Allocation")