HSAs 2026: Maximizing Health Savings and Investment Growth

Anúncios

Health Savings Accounts (HSAs) have long been lauded as one of the most powerful financial tools available to American families, offering a unique blend of tax advantages and healthcare savings. As we look ahead to 2026, understanding the latest HSA 2026 updates is paramount for maximizing these benefits. These accounts are not just for covering immediate medical expenses; they are potent investment vehicles that can significantly bolster your long-term financial security, especially in retirement.

The landscape of healthcare and personal finance is constantly evolving, and HSAs are no exception. Each year brings potential adjustments to contribution limits, eligibility requirements, and investment opportunities. For 2026, experts anticipate several key changes that will influence how individuals and families approach their health savings strategies. Staying informed about these HSA 2026 updates is crucial for making the most out of your account.

Anúncios

This comprehensive guide delves into everything you need to know about HSAs in 2026. We’ll explore the anticipated contribution limit increases, delve into expanded investment avenues, clarify eligibility criteria, and provide actionable strategies to optimize your HSA for both current healthcare needs and future financial goals. Whether you’re a seasoned HSA user or considering opening one for the first time, this article will equip you with the knowledge to navigate the 2026 HSA environment effectively.

Understanding the Core Benefits of an HSA

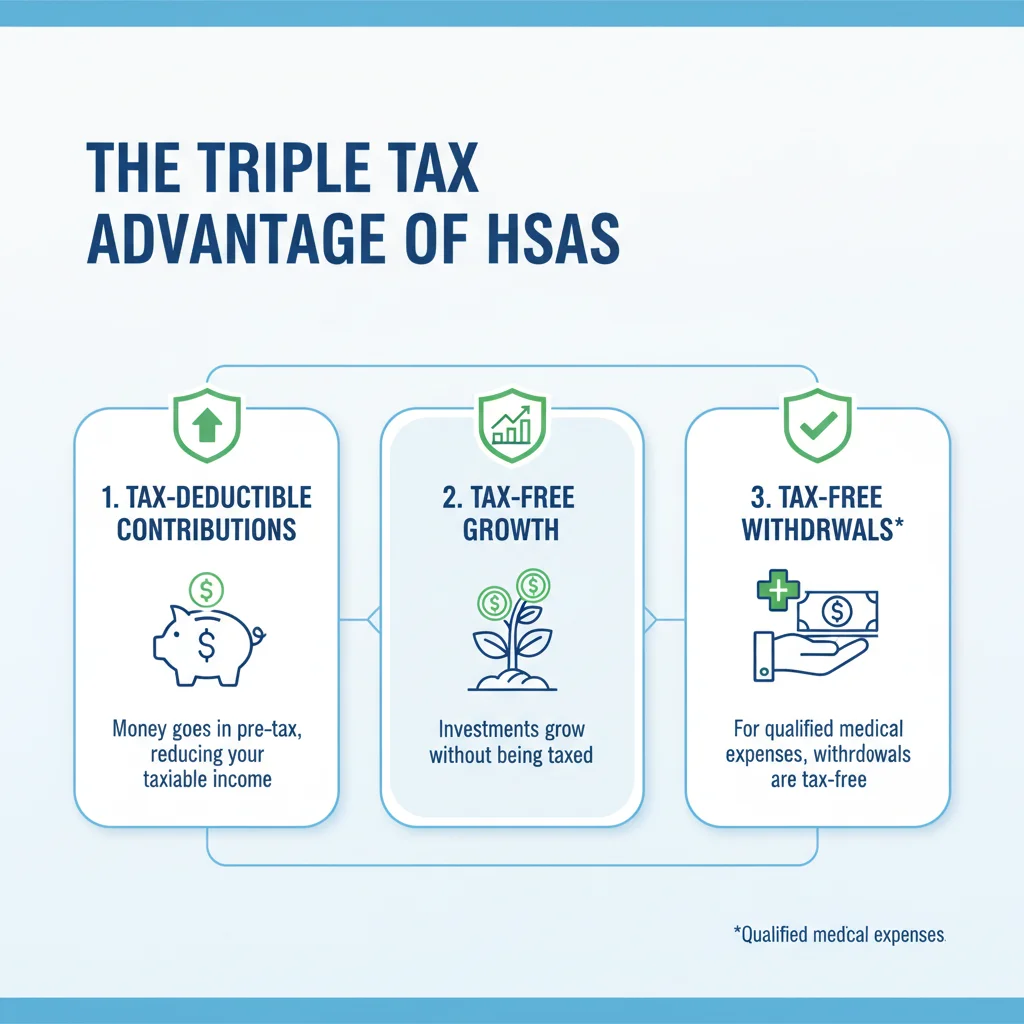

Before diving into the specifics of the HSA 2026 updates, it’s essential to revisit the fundamental advantages that make these accounts so attractive. HSAs offer a ‘triple tax advantage,’ a benefit rarely found in other savings or investment vehicles:

- Tax-Deductible Contributions: Money you contribute to an HSA is tax-deductible, reducing your taxable income in the year you make the contribution. This is an immediate tax saving that can be substantial.

- Tax-Free Growth: Any earnings from investments within your HSA grow tax-free. This means dividends, interest, and capital gains are not taxed as long as they remain in the account, allowing your money to compound more rapidly.

- Tax-Free Withdrawals: When you use HSA funds for qualified medical expenses, the withdrawals are entirely tax-free. This includes a wide range of expenses, from doctor’s visits and prescriptions to dental care and vision services.

Beyond these tax benefits, HSAs offer unparalleled flexibility. Unlike Flexible Spending Accounts (FSAs), HSA funds roll over from year to year, never expiring. This allows you to build a substantial balance over time, which can be particularly beneficial for retirement planning, as we will discuss later.

Anúncios

Anticipated HSA 2026 Contribution Limit Increases

One of the most eagerly awaited HSA 2026 updates concerns the contribution limits. These limits are adjusted annually for inflation, and while the exact figures for 2026 are typically announced later in the preceding year, we can project based on historical trends and economic forecasts. Increased limits mean individuals and families can save even more, amplifying the tax benefits and investment potential.

Individual Coverage vs. Family Coverage

HSA contribution limits differ based on whether you have individual (self-only) or family coverage under a High Deductible Health Plan (HDHP). For 2025, the individual limit is $4,150 and the family limit is $8,300. Based on inflation projections, it’s reasonable to expect these figures to rise for 2026. For illustrative purposes, if inflation continues at a moderate pace, we might see individual limits approaching $4,300-$4,400 and family limits in the range of $8,600-$8,800 or even higher. These are estimates, and official numbers will be released by the IRS.

Catch-Up Contributions for Those 55 and Older

Another crucial aspect of HSA contributions is the catch-up contribution. Individuals aged 55 and older can contribute an additional amount each year beyond the standard limit. This provision is designed to help older adults bolster their health savings as they approach retirement. The catch-up contribution for 2025 remains at $1,000, and it is generally not indexed for inflation in the same way as the standard limits. Therefore, it is expected to remain $1,000 for 2026. This extra contribution is a significant advantage for those nearing retirement, allowing them to accumulate funds more rapidly.

Understanding these potential increases is vital for budget planning and optimizing your contributions. Maximizing your contributions each year is a cornerstone of a robust HSA strategy, especially with the HSA 2026 updates providing more room to save.

Navigating Eligibility for an HSA in 2026

Eligibility is the first hurdle for anyone looking to open and contribute to an HSA. The core requirement is enrollment in a High Deductible Health Plan (HDHP). The IRS defines specific minimum deductible and maximum out-of-pocket limits for HDHPs that qualify for HSA eligibility. These thresholds also see annual adjustments, and the HSA 2026 updates will likely include revised figures.

HDHP Requirements for 2026

For 2025, an HDHP must have a minimum annual deductible of $1,650 for self-only coverage and $3,300 for family coverage. The maximum out-of-pocket expenses (including deductibles, co-payments, and co-insurance, but not premiums) cannot exceed $8,300 for self-only coverage and $16,600 for family coverage. For 2026, we can anticipate slight increases in these figures due to inflation. These changes are part of the broader HSA 2026 updates and are important to monitor when selecting your health insurance plan.

Other Eligibility Criteria

- You cannot be covered by any other health plan that is not an HDHP (with some exceptions, such as specific disease insurance or accident insurance).

- You cannot be enrolled in Medicare.

- You cannot be claimed as a dependent on someone else’s tax return.

It’s crucial to review your health insurance plan annually to ensure it continues to meet the HDHP requirements for HSA eligibility. A lapse in eligibility could impact your ability to contribute or even necessitate withdrawing excess contributions, potentially incurring penalties.

Expanded Investment Opportunities for HSAs in 2026

While often viewed primarily as savings accounts for healthcare expenses, HSAs truly shine as investment vehicles. The tax-free growth component means that the longer your money remains invested, the more it can compound, significantly increasing your financial reserves. The HSA 2026 updates are expected to continue the trend of offering more diverse and accessible investment options.

Many HSA providers now offer a wide range of investment choices, from low-cost index funds and exchange-traded funds (ETFs) to individual stocks and bonds. This allows account holders to tailor their investment strategy to their risk tolerance and financial goals. For 2026, we might see:

- Broader Fund Selection: More providers are likely to expand their offerings to include a greater variety of mutual funds, including ESG (Environmental, Social, and Governance) options, catering to diverse investor preferences.

- Lower Fees: Increased competition among HSA administrators is driving down administrative and investment fees, making it more cost-effective to invest your HSA funds. Lower fees mean more of your money goes towards growth.

- Improved Digital Platforms: User-friendly online platforms and mobile apps are becoming standard, offering easier access to manage investments, track performance, and make informed decisions.

- Guidance and Robo-Advisors: Some HSA providers are integrating robo-advisory services or providing more robust educational resources to help account holders, especially those new to investing, make strategic choices.

Strategic Investment Approaches for Your HSA

When approaching HSA investments, consider these strategies:

- Long-Term Growth: If you’re relatively healthy and can pay for current medical expenses out-of-pocket, consider investing a significant portion of your HSA funds for long-term growth. This allows the tax-free compounding to work its magic over decades.

- Diversification: Just like any other investment portfolio, diversify your HSA investments across different asset classes to mitigate risk.

- Risk Tolerance: Align your investment choices with your personal risk tolerance. Younger individuals with a longer time horizon might opt for more aggressive growth-oriented investments, while those closer to retirement might choose a more conservative approach.

- Review Regularly: Periodically review your investment performance and adjust your strategy as needed, especially in response to market changes or personal financial milestones.

The HSA 2026 updates in investment options present an excellent opportunity to fine-tune your strategy and ensure your account is working as hard as possible for your financial future.

Maximizing Your HSA for Retirement Planning

One of the most powerful, yet often underutilized, aspects of an HSA is its potential as a retirement savings vehicle. Many financial experts refer to it as a ‘super 401(k)’ or ‘super IRA’ due to its unique tax advantages. By treating your HSA not just as a spending account but as an investment account for future healthcare costs, you can significantly enhance your retirement security.

The ‘Retirement Healthcare Account’ Strategy

The ideal strategy for maximizing your HSA for retirement involves:

- Maxing Out Contributions: Contribute the maximum allowable amount each year, including catch-up contributions if you’re eligible.

- Paying for Current Medical Expenses Out-of-Pocket: Whenever possible, pay for your current medical expenses using other funds (e.g., your regular checking account) and save your receipts. This allows your HSA funds to remain invested and grow tax-free.

- Investing for Growth: As discussed, invest your HSA funds in a diversified portfolio geared for long-term growth.

- Reimbursement in Retirement: In retirement, you can then withdraw funds tax-free to reimburse yourself for all the qualified medical expenses you paid out-of-pocket throughout your working life. This essentially creates a tax-free income stream in retirement.

Even if you don’t save every receipt, HSA funds can be used for qualified medical expenses in retirement, including Medicare premiums, long-term care insurance premiums, and other out-of-pocket costs, all tax-free. After age 65, you can also withdraw HSA funds for non-medical expenses, though these withdrawals will be subject to ordinary income tax (similar to a traditional IRA or 401(k)), but without the 20% penalty typically applied before age 65. This flexibility makes HSAs an incredibly versatile tool for retirement.

HSA 2026 Updates: Impact on US Families

The HSA 2026 updates carry significant implications for US families, offering opportunities to enhance their financial well-being and prepare for rising healthcare costs. For families, the higher contribution limits for family coverage are particularly beneficial, allowing for a larger pool of tax-advantaged savings and investments.

Planning for Family Healthcare Needs

Families often face higher and more unpredictable healthcare expenses than individuals. An HSA provides a critical buffer against these costs. By contributing the maximum family limit, families can build a substantial fund to cover deductibles, co-pays, prescriptions, and even dental and vision care for all dependents.

The ability to invest these funds means that a family’s HSA can grow into a significant asset over time, potentially covering future college-related health expenses for children or serving as a vital resource for older parents’ medical needs. The HSA 2026 updates reinforce the value of these accounts as a cornerstone of family financial planning.

Education and Awareness

One of the challenges with HSAs is a lack of widespread understanding of their full potential. Many people view them merely as spending accounts, missing out on the powerful investment and retirement planning benefits. Financial advisors and employers play a crucial role in educating families about the comprehensive advantages of HSAs, especially in light of the HSA 2026 updates.

Families should take the time to understand their HDHP, evaluate their healthcare spending patterns, and strategize how to best utilize their HSA. This might involve setting up automated contributions, choosing appropriate investment options, and keeping meticulous records of medical expenses for future tax-free reimbursements.

Strategies for Optimizing Your HSA in 2026

With the anticipated HSA 2026 updates, now is the perfect time to optimize your strategy. Here are actionable tips to get the most out of your Health Savings Account:

- Automate Maximum Contributions: Set up automatic contributions from your paycheck or bank account to ensure you hit the maximum allowable limit for 2026. Consistency is key to long-term growth.

- Separate Savings from Investments: Consider keeping a small portion of your HSA in a readily accessible savings option for immediate medical needs (e.g., your deductible), and invest the remainder for long-term growth.

- Leverage Employer Contributions: Many employers contribute to their employees’ HSAs as part of their benefits package. Ensure you’re taking full advantage of any employer match or contributions, as this is essentially free money.

- Understand Qualified Medical Expenses: Familiarize yourself with what constitutes a qualified medical expense according to IRS guidelines. This includes a wide array of services and products, from prescription medications and chiropractic care to eyeglasses and even certain over-the-counter items with a doctor’s prescription.

- Keep Meticulous Records: If you plan to pay for current medical expenses out-of-pocket to allow your HSA to grow, keep detailed records (receipts, EOBs) of all qualified medical expenses. This will be crucial for tax-free reimbursements in the future.

- Review Investment Performance: Regularly check the performance of your HSA investments. Adjust your portfolio as needed to align with your financial goals and risk tolerance.

- Consider Beneficiary Designations: Just like other retirement accounts, designate beneficiaries for your HSA. This ensures that the funds are transferred according to your wishes in the event of your passing.

- Stay Informed: Continue to monitor official IRS announcements regarding HSA limits and rules, as well as any further HSA 2026 updates.

The Future of HSAs and Healthcare

The evolution of HSAs reflects a broader trend in healthcare towards consumer-driven models, where individuals take a more active role in managing their health expenses and financial well-being. As healthcare costs continue to rise, the importance of tools like HSAs will only grow.

Looking beyond the immediate HSA 2026 updates, we can anticipate further enhancements and integrations. Technology will likely play an even larger role, with more sophisticated apps and platforms helping users track expenses, manage investments, and even connect with healthcare providers. Policy discussions may also continue around expanding HSA eligibility or adjusting contribution rules to make them even more accessible and beneficial to a wider segment of the population.

For US families, the strategic use of an HSA in 2026 and beyond is not just about saving money; it’s about empowering them to make informed healthcare decisions, build a robust financial safety net, and secure a healthier, more prosperous future. The triple tax advantage, combined with investment opportunities and portability, makes HSAs an indispensable component of modern financial planning. By staying proactive and leveraging the HSA 2026 updates, you can position yourself and your family for optimal health and financial outcomes.

Conclusion: Embracing the HSA 2026 Updates for Financial Well-being

The HSA 2026 updates represent a continued commitment to providing American families with powerful tools to manage their healthcare costs and build long-term wealth. With anticipated increases in contribution limits and potentially enhanced investment opportunities, HSAs remain an unparalleled financial instrument.

By understanding the eligibility requirements, maximizing your contributions, and strategically investing your funds, you can leverage your HSA to cover current medical expenses, save for future healthcare needs, and even bolster your retirement savings. The triple tax advantage—tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses—makes HSAs a cornerstone of smart financial planning.

Don’t let the complexities deter you. Take the time to educate yourself on the latest HSA 2026 updates, consult with a financial advisor if needed, and make a conscious effort to integrate your HSA into your overall financial strategy. For US families, the benefits extend far beyond immediate healthcare savings, offering a pathway to greater financial security and peace of mind in an ever-changing economic and healthcare landscape. Start planning today to unlock the full potential of your Health Savings Account in 2026 and for years to come.

2026: Contribution Limits & Smart Allocation")