Mastering 529 College Savings Plans in 2026: New Rules & Benefits

Anúncios

Preparing for the rising costs of higher education is a daunting task for many families across the United States. Fortunately, 529 college savings plans have long stood as a cornerstone of educational financial planning, offering significant tax advantages to help parents and guardians build a nest egg for their children’s future. As we approach 2026, the landscape of these vital savings vehicles continues to evolve, bringing with it new rules, expanded benefits, and fresh opportunities for savvy investors. Understanding these changes is not just beneficial; it’s essential for maximizing your savings potential and ensuring your loved ones have access to the education they deserve. This comprehensive guide delves into the intricacies of 529 College Savings 2026, providing an in-depth look at what’s new, what’s improved, and how you can strategically leverage these plans.

The journey to higher education is often paved with financial considerations that can seem overwhelming. From tuition fees and housing to books and technology, the expenses accumulate rapidly. This is where 529 plans shine, offering a tax-advantaged way to save for these qualified education expenses. For years, these plans have been praised for their flexibility and the growth potential they offer. However, the world of financial planning is dynamic, and legislative updates frequently reshape the tools available to us. The year 2026 is poised to introduce several key modifications to 529 plans, impacting everything from contribution limits to eligible expenses and even how unused funds can be utilized. Staying abreast of these developments is crucial for optimizing your college savings strategy.

This article aims to be your definitive resource for navigating the exciting changes surrounding 529 College Savings 2026. We will explore the legislative backdrop influencing these updates, detail the specific new rules and benefits, and offer practical strategies for integrating these changes into your existing or prospective 529 plan. Whether you are a new parent just starting to think about college savings or a seasoned investor looking to fine-tune your approach, the insights provided here will equip you with the knowledge needed to make informed decisions. Let’s embark on this journey to demystify the future of college savings.

Anúncios

The Evolution of 529 College Savings Plans: A Historical Perspective

Before diving into the specifics of 529 College Savings 2026, it’s helpful to understand the historical context and foundational principles of these plans. Established under Section 529 of the Internal Revenue Code, these qualified tuition plans were designed to encourage saving for future education costs. Initially, their primary benefit was tax-free growth and tax-free withdrawals for qualified higher education expenses. Over the years, their scope has broadened significantly, adapting to the evolving needs of students and families.

Key Milestones in 529 Plan Development:

- 1996: The Small Business Job Protection Act created 529 plans, initially allowing tax-deferred growth on contributions.

- 2001: The Economic Growth and Tax Relief Reconciliation Act made withdrawals for qualified education expenses tax-free, a monumental change that cemented their popularity.

- 2006: The Pension Protection Act made the tax-free withdrawal provision permanent.

- 2015: The ABLE Act expanded qualified expenses to include computer equipment, software, and internet access.

- 2017: The Tax Cuts and Jobs Act allowed 529 funds to be used for K-12 private school tuition, up to $10,000 per student per year.

- 2019: The SECURE Act further expanded qualified expenses to include student loan repayments (up to $10,000 lifetime per beneficiary) and apprenticeship program costs.

- 2022: The SECURE Act 2.0 introduced the groundbreaking provision allowing unused 529 funds to be rolled over into a Roth IRA, albeit with specific limitations.

Each legislative update has progressively enhanced the utility and flexibility of 529 plans, making them more attractive and versatile financial instruments. These historical changes underscore a consistent legislative intent: to provide robust, tax-advantaged tools for educational savings. As we look towards 2026, this trend of enhancement and adaptation is expected to continue, further solidifying the role of 529 plans in a comprehensive financial strategy for education. The ongoing evolution reflects a commitment to addressing the dynamic landscape of educational funding and providing more avenues for families to achieve their academic goals without being burdened by excessive debt. This proactive approach ensures that 529 College Savings 2026 remains a powerful and relevant tool for future generations.

Anúncios

New Rules and Regulations for 529 College Savings in 2026

The year 2026 is anticipated to bring forth several significant updates to 529 college savings plans, building upon the foundations laid by previous legislation. While specific details can always be subject to final legislative approval, the general direction points towards greater flexibility, expanded eligible expenses, and potentially new contribution incentives. Understanding these prospective changes is key to optimizing your 529 College Savings 2026 strategy.

Expanded Definition of Qualified Education Expenses:

One of the most impactful changes expected for 2026 is a further expansion of what constitutes a “qualified education expense.” This could include:

- Broader Scope for Vocational and Trade Schools: While already partially covered, 2026 may see an even more inclusive definition that encompasses a wider array of certifications, tools, and materials for vocational and trade programs, reflecting the growing importance of skilled trades in the economy.

- Professional Development and Continuing Education: There’s a strong possibility that 529 funds could become more widely applicable to professional development courses, certifications, and continuing education units required for career advancement, even for individuals already in the workforce. This would allow 529 plans to support lifelong learning beyond traditional undergraduate degrees.

- Enhanced Support for Special Needs Education: Further provisions may be introduced to cover a broader range of expenses related to special needs education, including specialized therapies, adaptive equipment, and personalized learning support systems, ensuring that 529 plans are even more inclusive.

Adjustments to Contribution Limits and Tax Deductions:

While federal 529 contributions do not have an annual limit, they are subject to gift tax rules. State-level plans often have overall maximums. For 2026, we might see:

- Increased Annual Gift Tax Exclusion: The IRS typically adjusts the annual gift tax exclusion periodically. An increase in 2026 would allow individuals to contribute more to a 529 plan without incurring gift tax implications or needing to file a gift tax return.

- Potential for Enhanced State Tax Benefits: Many states offer income tax deductions or credits for contributions to their 529 plans. While these are state-specific, there could be a legislative push to standardize or enhance these benefits across more states, making 529 plans even more attractive at the local level.

The Roth IRA Rollover Provision (SECURE Act 2.0 Refinements):

The ability to roll over unused 529 funds into a Roth IRA, introduced by the SECURE Act 2.0, is a game-changer. For 2026, it’s possible we’ll see refinements or clarifications to this rule:

- Clarification on Rollover Limits and Age Requirements: While the current rule allows rollovers up to the annual Roth IRA contribution limit (with a lifetime cap of $35,000 and the 529 account needing to be open for 15 years), 2026 might bring clearer guidance or slight adjustments to these parameters.

- Streamlined Process: There might be efforts to simplify the administrative process for these rollovers, making it easier for beneficiaries to transition unused funds into their retirement savings without unnecessary hurdles. This flexibility ensures that funds not used for education can still benefit the beneficiary’s financial future, reducing the fear of over-saving in a 529 plan.

These anticipated changes underscore a legislative commitment to making 529 plans more adaptable and beneficial for a wider range of educational and financial scenarios. As these proposals solidify into law, they will undoubtedly shape how families approach 529 College Savings 2026.

Benefits of 529 College Savings Plans in 2026

Beyond the new rules, the core benefits that make 529 plans so attractive will continue to be a cornerstone of educational financial planning in 2026. These advantages, combined with the anticipated updates, reinforce the position of 529 plans as one of the most powerful tools available for college savings.

Tax-Free Growth and Withdrawals:

The hallmark of 529 plans remains their incredible tax efficiency. Contributions grow tax-free, and withdrawals for qualified education expenses are also tax-free at the federal level. Many states also offer similar tax benefits. This means that every dollar earned through investment growth can be put towards education, rather than being eroded by taxes. Over an extended saving period, this tax-free compounding can significantly boost the overall value of your college fund, often surpassing what could be achieved in a taxable investment account.

Flexibility in Use of Funds:

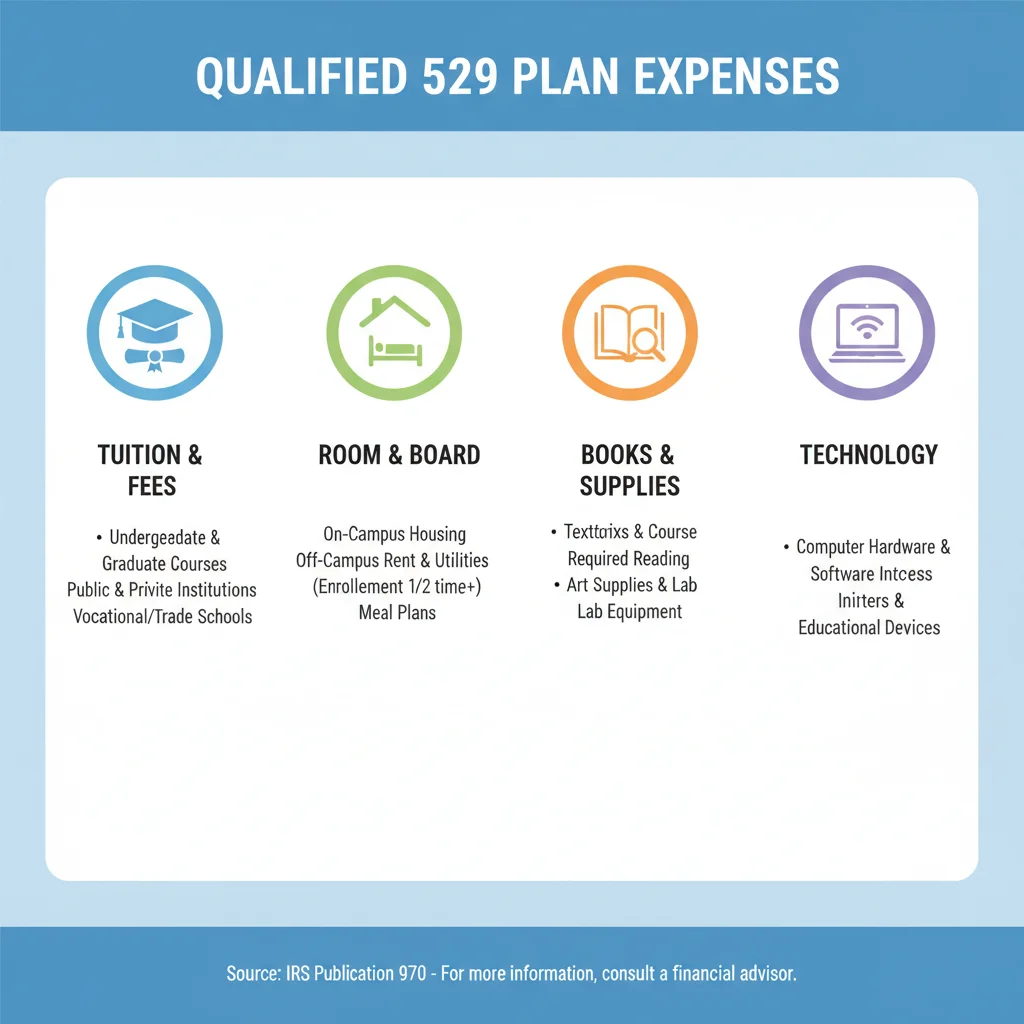

The expanded definition of qualified expenses, as discussed for 529 College Savings 2026, enhances the inherent flexibility of these plans. Funds can be used for a wide range of costs at eligible educational institutions, including:

- Tuition and fees at colleges, universities, and vocational schools.

- Room and board for students enrolled at least half-time.

- Books, supplies, and equipment required for enrollment.

- Computer equipment, software, and internet access.

- K-12 private school tuition (up to $10,000 per year per student).

- Student loan repayments (up to $10,000 lifetime per beneficiary).

- Apprenticeship program expenses.

This broad scope ensures that 529 plans can adapt to various educational paths and financial needs, making them a versatile choice for families.

Ownership and Control:

Unlike some other savings vehicles, the account owner (typically the parent or grandparent) retains control over the 529 account. This means you decide when and how the funds are disbursed. You can also change the beneficiary to another eligible family member if the original beneficiary decides not to pursue higher education or receives a scholarship. This level of control provides peace of mind and adaptability.

Impact on Financial Aid:

One common concern is how 529 plans affect eligibility for financial aid. Generally, 529 plans are treated favorably in the financial aid calculation process:

- Parent-Owned 529s: Funds in a parent-owned 529 plan are considered a parental asset on the Free Application for Federal Student Aid (FAFSA). Only a small percentage (typically a maximum of 5.64%) of these assets are counted towards the Expected Family Contribution (EFC). This is significantly less impactful than student-owned assets, which are assessed at 20%.

- Grandparent-Owned 529s: Under the FAFSA Simplification Act, grandparent-owned 529 plans no longer count as income for the student, making them an even more attractive option for extended family members wishing to contribute.

This favorable treatment helps ensure that saving for college doesn’t unduly penalize families when it comes to qualifying for need-based financial aid, reinforcing the strategic advantage of 529 College Savings 2026.

Strategic Planning with 529 Plans in 2026

To fully leverage the benefits and navigate the new rules of 529 College Savings 2026, a strategic approach is essential. This involves understanding your options, making informed investment decisions, and adapting to potential changes in your family’s educational journey.

Choosing the Right 529 Plan:

There are two main types of 529 plans:

- College Savings Plans: These are investment accounts that allow your contributions to grow tax-free. They offer a variety of investment options, usually including age-based portfolios (which automatically adjust asset allocation as the beneficiary gets closer to college age) and static portfolios. Most states offer their own plans, and you are generally not required to use your home state’s plan, though doing so might offer state income tax benefits.

- Prepaid Tuition Plans: These plans allow you to lock in tuition rates at eligible in-state public colleges and universities. They are less common and typically have more restrictions.

For most families, a college savings plan offers greater flexibility and investment potential. When choosing, consider factors like investment options, fees, past performance, and state tax benefits.

Contribution Strategies:

Developing a consistent contribution strategy is vital. Even small, regular contributions can grow substantially over time due to compounding. Consider:

- Automated Contributions: Set up automatic transfers from your checking account to your 529 plan, ensuring consistency.

- Windfalls and Gifts: Direct bonuses, tax refunds, or monetary gifts from relatives into the 529 plan. Remember the gift tax exclusion limits for large contributions.

- Front-Loading: Some families choose to “front-load” their 529 contributions by contributing a lump sum equivalent to five years’ worth of annual gift tax exclusions in one go. This allows more money to grow tax-free sooner.

Investment Considerations within Your 529 Plan:

The investment options within 529 plans vary by state and plan administrator. For 529 College Savings 2026, it’s crucial to:

- Assess Risk Tolerance: Younger beneficiaries allow for a more aggressive investment strategy, while older beneficiaries warrant a more conservative approach to protect accumulated savings. Age-based portfolios are designed to do this automatically.

- Review Performance and Fees: Regularly check the performance of your chosen investments and be aware of any associated fees, which can eat into your returns.

- Diversify: Even within a 529 plan, ensure your investments are diversified across different asset classes to mitigate risk.

Coordinating with Other Financial Aid and Savings:

A 529 plan should be part of a broader financial strategy. Consider how it integrates with:

- Scholarships and Grants: If your child receives scholarships, you can withdraw an equivalent amount from the 529 plan without incurring the 10% penalty (though earnings will be subject to income tax). This reduces the amount needed for qualified expenses from the 529.

- Student Loans: While 529s can cover student loan repayments, the goal should be to minimize the need for loans. A well-funded 529 can significantly reduce future student debt.

- Coverdell ESAs: For those with lower incomes, Coverdell Education Savings Accounts offer similar tax benefits but with lower contribution limits and stricter income requirements. They can be used in conjunction with 529 plans.

Leveraging the Roth IRA Rollover (Post-SECURE Act 2.0):

The ability to roll over unused 529 funds into a Roth IRA is a significant new benefit. For 529 College Savings 2026, plan carefully:

- Beneficiary’s Future: If it becomes clear that a beneficiary won’t use all the 529 funds for educational expenses, this rollover provides a valuable alternative to simply withdrawing funds and paying taxes and penalties.

- Retirement Planning: This feature seamlessly transitions education savings into retirement savings, offering a tax-free growth vehicle for the beneficiary’s long-term financial health. Remember the 15-year account age requirement and the $35,000 lifetime cap.

By thoughtfully applying these strategies, families can maximize the potential of their 529 plans and adapt to the changes expected in 2026 and beyond, ensuring a robust financial foundation for educational pursuits.

Potential Challenges and Considerations for 529 College Savings in 2026

While 529 plans offer numerous advantages, it’s important to be aware of potential challenges and considerations that might arise, especially with the evolving landscape of 529 College Savings 2026. Understanding these nuances allows for proactive planning and mitigation of potential drawbacks.

Investment Risk:

Like any investment, 529 plans are subject to market fluctuations. While they offer tax-free growth, the value of your account can decrease depending on the performance of the underlying investments. This is particularly relevant for beneficiaries nearing college age, where a sudden market downturn could significantly impact available funds. Diversification and age-based portfolios are designed to mitigate this, but risk can never be entirely eliminated. Regularly reviewing your investment strategy and making adjustments as your child approaches college is crucial.

Non-Qualified Withdrawals:

If funds are withdrawn from a 529 plan for non-qualified expenses, the earnings portion of the withdrawal will be subject to federal income tax and a 10% federal penalty tax. Some states may also levy their own taxes and penalties. While the Roth IRA rollover provision (discussed earlier) offers a valuable escape route for unused funds, it’s vital to clearly understand what constitutes a qualified expense to avoid these penalties. The expanded definition of qualified expenses in 2026 aims to reduce this risk, but careful attention is still required.

State-Specific Rules and Benefits:

Each state administers its own 529 plan, and while federal rules apply universally, state-specific rules, benefits, and investment options can vary significantly. For instance, some states offer generous income tax deductions for contributions, but only if you invest in their in-state plan. Others might allow you to invest in any state’s plan and still receive a tax benefit. It’s crucial to research your home state’s plan and compare it with others, especially if state tax benefits are a significant factor in your decision-making for 529 College Savings 2026.

Inflation and College Cost Increases:

Despite the tax advantages, the rising cost of college often outpaces inflation, and even robust investment growth within a 529 plan can sometimes struggle to keep pace with tuition increases. It’s important to set realistic savings goals and regularly review them. While 529 plans are an excellent tool, they may need to be supplemented by other savings strategies or financial aid to fully cover all educational costs.

Changes in Beneficiary Plans:

Life happens, and a child’s educational path may change. They might decide not to attend college, choose a less expensive option, or receive substantial scholarships. While 529 plans offer flexibility to change beneficiaries or roll funds into a Roth IRA, these actions come with their own rules and potential limitations. Understanding these contingencies upfront can help you make more adaptable savings decisions.

Complexity of Rules:

The evolving nature of 529 plans, with new legislation like the SECURE Act 2.0 and anticipated changes in 2026, can make the rules complex. Keeping up with these updates and understanding their implications requires ongoing attention. Consulting with a qualified financial advisor specializing in education planning can be invaluable in navigating these complexities and ensuring your 529 College Savings 2026 strategy is optimal.

By being mindful of these potential challenges, families can approach 529 planning with a more comprehensive perspective, allowing them to harness the full power of these plans while minimizing potential downsides.

The Role of Financial Advisors in 529 College Savings 2026

Given the complexity of financial planning and the continuous evolution of regulations, the role of a qualified financial advisor becomes increasingly critical, especially when navigating the nuances of 529 College Savings 2026. A knowledgeable advisor can provide personalized guidance, helping families make informed decisions that align with their unique financial situation and educational goals.

Expertise in Evolving Regulations:

Financial advisors stay abreast of the latest legislative changes, including those impacting 529 plans. They can interpret the new rules for 2026, such as expanded qualified expenses or refinements to the Roth IRA rollover, and explain how these apply to your specific circumstances. This expertise ensures you are taking full advantage of all available benefits and avoiding potential pitfalls.

Personalized Plan Selection:

With nearly every state offering multiple 529 plan options, choosing the right one can be overwhelming. An advisor can help you compare plans across different states, considering factors like investment options, fees, performance history, and, crucially, your home state’s tax benefits. They can assess which plan best suits your risk tolerance, time horizon, and financial objectives.

Optimizing Contribution Strategies:

An advisor can assist in developing a sustainable contribution strategy, taking into account your current income, expenses, and other financial goals. They can help you determine appropriate contribution amounts, advise on lump-sum contributions versus regular payments, and guide you through the implications of gift tax rules. Furthermore, they can help you integrate your 529 contributions with other savings vehicles and overall financial planning.

Investment Management within the 529:

Choosing the right investment portfolio within a 529 plan is crucial for maximizing growth. Advisors can help you select appropriate age-based or static portfolios based on your beneficiary’s age and your risk comfort level. They can also provide ongoing monitoring and recommend adjustments as market conditions change or as your child progresses towards college, ensuring your investments remain aligned with your goals for 529 College Savings 2026.

Coordination with Other Financial Aid and Planning:

A holistic financial plan considers all aspects of your financial life. An advisor can help integrate your 529 plan with your broader financial strategy, including retirement savings, insurance, estate planning, and understanding its impact on potential financial aid eligibility. They can also advise on how to strategically use 529 funds alongside scholarships, grants, and student loans to minimize overall educational costs and debt.

Navigating Unused Funds and Beneficiary Changes:

Should your beneficiary’s educational plans change, an advisor can guide you through the options, such as changing the beneficiary to another eligible family member or utilizing the Roth IRA rollover provision. They can help you understand the tax implications and ensure you make the most advantageous decision for your family’s financial future, especially with the evolving rules around 529 College Savings 2026.

In essence, a financial advisor acts as a trusted partner, simplifying complex decisions and providing clarity in the often intricate world of college savings. Their expertise can be invaluable in ensuring your 529 plan is a robust and effective tool for achieving your educational funding goals.

Conclusion: Embracing the Future of 529 College Savings in 2026

The landscape of educational funding is perpetually in motion, and 529 College Savings 2026 represents another significant chapter in the evolution of these powerful savings vehicles. From historical enhancements that broadened their scope to the anticipated new rules and benefits, 529 plans continue to adapt, offering increasingly versatile and tax-efficient ways for families to save for higher education.

The expected changes in 2026, including expanded definitions of qualified expenses, potential adjustments to contribution incentives, and refinements to the Roth IRA rollover provision, underscore a legislative commitment to making college savings more accessible, flexible, and responsive to modern educational pathways. These updates are designed not just to help families meet the rising costs of traditional four-year degrees but also to support vocational training, professional development, and even provide a robust financial safety net for unused funds.

For parents, guardians, and anyone committed to funding future education, the message is clear: 529 plans remain an indispensable tool. Their core benefits—tax-free growth, tax-free withdrawals for qualified expenses, and favorable treatment in financial aid calculations—are being continuously strengthened. However, maximizing these advantages requires proactive engagement. It means staying informed about the latest regulations, critically evaluating your investment choices, and strategically integrating your 529 plan into a comprehensive financial strategy.

As you plan for 529 College Savings 2026 and beyond, remember to:

- Research and Compare: Explore different state plans to find one that aligns best with your financial goals and offers advantageous state tax benefits if applicable.

- Contribute Consistently: Leverage the power of compounding by making regular, automated contributions, or strategically utilize windfalls.

- Review and Adjust: Revisit your investment strategy annually and adjust your risk tolerance as your beneficiary ages. Keep abreast of any further legislative changes that may impact your plan.

- Consider Professional Guidance: Don’t hesitate to consult a financial advisor. Their expertise can be invaluable in navigating the complexities, optimizing your plan, and ensuring it aligns with your overall financial objectives.

The dream of higher education should not be overshadowed by financial anxieties. By understanding and strategically utilizing the enhanced 529 College Savings 2026 plans, families can build a robust financial foundation, paving the way for a brighter, more educated future for the next generation. Start planning today, stay informed, and empower your loved ones with the gift of education.