The Digital Dollar in 2026: Economic Impact & Future Outlook of CBDC

The Digital Dollar in 2026: Exploring the Economic Implications of a Central Bank Digital Currency

Anúncios

The financial world is on the cusp of a monumental transformation, with the concept of a Central Bank Digital Currency (CBDC) gaining unprecedented traction globally. Among the most anticipated developments is the potential introduction of a digital dollar 2026. This isn’t merely an incremental upgrade to our existing payment systems; it represents a fundamental rethinking of money itself, with profound economic implications that will reverberate across all sectors of society. As we approach 2026, the discussions around the digital dollar are intensifying, driven by technological advancements, geopolitical shifts, and the evolving needs of a digital-first economy.

The idea of a digital dollar, issued and backed by the Federal Reserve, is designed to offer the benefits of digital payments while maintaining the stability and trust associated with a sovereign currency. Unlike cryptocurrencies such as Bitcoin or Ethereum, which are decentralized and volatile, a CBDC would be a direct liability of the central bank, much like physical cash. This distinction is crucial and underpins many of the economic arguments for and against its implementation.

In this comprehensive article, we will delve deep into the multifaceted economic implications of a digital dollar 2026. We will explore the potential benefits, including enhanced financial inclusion, improved payment efficiency, and new tools for monetary policy. Simultaneously, we will critically examine the challenges and risks, such as privacy concerns, cybersecurity threats, and the potential for disintermediation of commercial banks. Our goal is to provide an insider’s perspective on what the digital dollar could mean for individuals, businesses, and the broader economy as we look ahead to 2026 and beyond.

Anúncios

Understanding the Digital Dollar: What Exactly is it?

Before we dissect its economic ramifications, it’s essential to grasp what a digital dollar entails. A Central Bank Digital Currency (CBDC) is a digital form of a country’s fiat currency. For the United States, a digital dollar would be a digital representation of the US dollar, issued by the Federal Reserve. It would be distinct from existing digital payment methods like credit cards, debit cards, or peer-to-peer payment apps, which rely on commercial bank accounts. Instead, a digital dollar would be a direct claim on the central bank, much like physical cash.

There are generally two main models for CBDCs: retail and wholesale. A retail CBDC would be available for general public use, allowing individuals and businesses to hold accounts directly with the central bank or through intermediaries. A wholesale CBDC, on the other hand, would be restricted to financial institutions for interbank settlements and other wholesale transactions. The discussions around the digital dollar 2026 primarily revolve around a retail CBDC, given its potential for broader societal impact.

Anúncios

The technological backbone of a digital dollar could vary. While blockchain technology, popularized by cryptocurrencies, is a candidate, central banks are also exploring other distributed ledger technologies (DLT) or even centralized database systems. The key is to create a secure, resilient, and efficient digital payment infrastructure that can handle a high volume of transactions and meet the demands of a modern economy.

The motivations behind exploring a digital dollar are multi-faceted. They include maintaining monetary sovereignty in an increasingly digital world, promoting financial stability, enhancing payment system efficiency, fostering innovation, and addressing financial inclusion gaps. As various nations, including China with its digital yuan, advance their CBDC initiatives, the pressure on the US to define its stance on a digital dollar intensifies, making the digital dollar 2026 a critical point of focus for policymakers and economists alike.

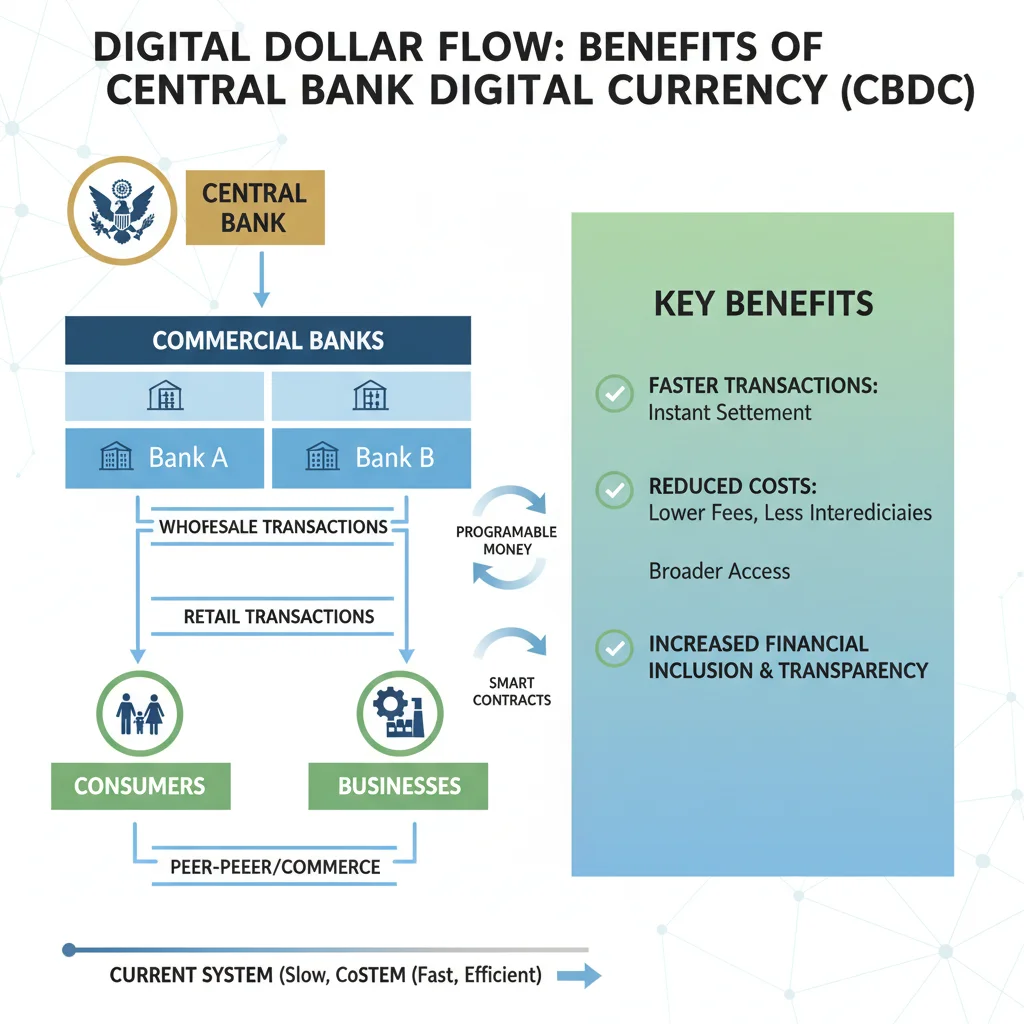

Economic Benefits of a Digital Dollar by 2026

The potential economic benefits of a fully implemented digital dollar 2026 are extensive and could fundamentally reshape the financial landscape. These benefits touch upon various aspects of economic life, from individual transactions to macroeconomic stability.

Enhanced Financial Inclusion

One of the most frequently cited benefits of a digital dollar is its potential to improve financial inclusion. Millions of Americans are unbanked or underbanked, meaning they lack access to traditional banking services. A digital dollar could provide a low-cost, accessible alternative for these populations, enabling them to participate more fully in the digital economy. Imagine a system where everyone has access to a basic digital account, allowing them to send and receive payments, store value, and access financial services without the need for a traditional bank account. This could significantly reduce reliance on costly alternative financial services like check-cashing stores and payday lenders, thereby empowering vulnerable communities.

Improved Payment Efficiency and Lower Costs

Current payment systems, while generally efficient, still incur significant costs and can be slow, especially for cross-border transactions. A digital dollar could streamline payments, making them faster, cheaper, and more efficient. Instantaneous settlement, reduced intermediary fees, and 24/7 availability could benefit businesses and consumers alike. This efficiency gain could translate into lower operating costs for businesses, potentially leading to lower prices for consumers and increased economic activity. The real-time nature of transactions could also improve cash flow management for businesses, especially small and medium-sized enterprises (SMEs).

New Tools for Monetary Policy

A digital dollar could equip the Federal Reserve with new and powerful tools for conducting monetary policy. In times of economic crisis, for instance, direct fiscal stimulus could be disbursed more rapidly and precisely to individuals, bypassing traditional banking channels that can sometimes be slow. Furthermore, the ability to potentially pay interest on digital dollar holdings could give the central bank a new lever to influence savings and spending behavior, offering a more granular approach to managing inflation and stimulating economic growth. This could lead to more effective and responsive economic stabilization policies, crucial for navigating future economic downturns.

Strengthening the Dollar’s International Role

In an increasingly digital global economy, the widespread adoption of CBDCs by other major economies, particularly China, poses a potential challenge to the US dollar’s status as the world’s primary reserve currency. By introducing its own digital dollar, the US could reinforce the dollar’s international role, ensuring its continued relevance and dominance in cross-border trade and finance. A digital dollar could offer a more efficient and secure medium for international transactions, potentially making it more attractive than other digital currencies or existing correspondent banking networks.

Fostering Innovation

The introduction of a digital dollar could spur a wave of innovation in the financial technology (fintech) sector. By providing a foundational digital currency, it could enable the development of new financial products and services built on top of this infrastructure. This could lead to more competitive markets, greater choice for consumers, and the emergence of novel solutions for payments, lending, and investment. The interoperability of a digital dollar with existing and future financial technologies would be key to unlocking this innovation potential.

Challenges and Risks Associated with the Digital Dollar in 2026

While the potential benefits of a digital dollar 2026 are compelling, its implementation also presents significant challenges and risks that must be carefully addressed. These concerns span privacy, cybersecurity, financial stability, and the structure of the banking system.

Privacy Concerns

One of the most prominent concerns revolves around privacy. Unlike physical cash, which offers anonymity, digital transactions leave a digital footprint. A central bank-issued digital dollar raises questions about the extent to which the government could monitor individual spending habits. Striking the right balance between privacy for users and the need to combat illicit activities like money laundering and terrorist financing will be a complex task. Robust privacy protections, perhaps through cryptographic techniques or a tiered access system, would be essential to ensure public trust and adoption.

Cybersecurity Threats and System Resilience

A nationwide digital dollar system would represent a critical piece of national infrastructure, making it an attractive target for cyberattacks. The system would need to be exceptionally resilient, secure, and capable of withstanding sophisticated threats from state-sponsored actors and cybercriminals. A breach could have catastrophic consequences, undermining public confidence in the currency and potentially destabilizing the entire financial system. Investing heavily in cybersecurity measures, redundancy, and incident response protocols would be paramount.

Disintermediation of Commercial Banks

The introduction of a digital dollar could lead to the disintermediation of commercial banks. If individuals and businesses can hold accounts directly with the central bank, it could reduce the demand for commercial bank deposits, which are a primary source of funding for bank lending. This could impact banks’ profitability, their ability to provide credit, and potentially lead to a more concentrated banking sector. Policymakers would need to design the digital dollar in a way that complements, rather than competes with, the existing banking system, perhaps through a hybrid model where commercial banks act as intermediaries for central bank digital currency accounts.

Monetary Policy Implementation Challenges

While a digital dollar offers new monetary policy tools, it also introduces complexities. The ability to directly influence interest rates on digital dollar holdings could have unintended consequences for market liquidity and financial stability. Furthermore, in a crisis, a flight to the safety of central bank digital dollar accounts could exacerbate bank runs during periods of financial stress, potentially destabilizing the commercial banking sector. Careful calibration and robust regulatory frameworks would be necessary to manage these risks effectively.

International Implications and Geopolitics

The global race to develop CBDCs has significant geopolitical implications. If the US lags behind, it could risk losing its financial influence on the world stage. Conversely, the introduction of a digital dollar 2026 could trigger a global shift in payment systems and reserve currency dynamics. Coordinating with international partners and establishing common standards would be crucial to avoid fragmentation of the global financial system and to ensure the smooth functioning of cross-border payments.

The Road to a Digital Dollar in 2026: Key Considerations

The path to implementing a digital dollar 2026 is fraught with complex decisions and requires careful consideration of various factors. This is not a sprint, but a marathon that involves technological, legal, political, and economic hurdles.

Technological Infrastructure and Design

The choice of technological infrastructure is paramount. Should it be based on distributed ledger technology (DLT) or a centralized system? How will it ensure scalability, resilience, and security? The design must also consider interoperability with existing payment systems and future innovations. The Federal Reserve has been exploring various architectural models, and the final design will significantly impact the digital dollar’s functionality and acceptance.

Legal and Regulatory Framework

A digital dollar would necessitate a comprehensive legal and regulatory framework. This includes defining its legal status as a form of currency, addressing issues of data privacy and security, establishing consumer protection mechanisms, and clarifying the roles and responsibilities of various financial institutions. Legislation would be required to authorize its issuance and outline its operational parameters. This is a crucial step that will likely involve extensive debate and collaboration between Congress, the Treasury, and the Federal Reserve.

Public Acceptance and Education

The success of a digital dollar hinges on public acceptance. This requires not only a user-friendly and reliable system but also a robust public education campaign to explain its benefits, address concerns, and build trust. Many individuals may be wary of a new form of money, especially given the complexities surrounding digital currencies. Clear communication about privacy protections, security measures, and ease of use will be vital for widespread adoption.

International Cooperation and Standards

As other countries develop their own CBDCs, international cooperation becomes increasingly important. Establishing common standards and protocols for cross-border transactions involving digital currencies could facilitate global trade and reduce friction in international payments. The US would need to engage actively with international bodies and partner nations to shape the future of global digital finance and ensure the digital dollar’s interoperability with other CBDCs.

The Geopolitical Landscape and the Digital Dollar

The race to develop and implement CBDCs is not just an economic endeavor; it’s a geopolitical one. The nation that successfully issues a widely adopted and stable digital currency could gain significant influence in global finance. The digital dollar 2026 is therefore not just about domestic economic policy, but also about maintaining the US’s strategic position on the world stage.

Maintaining Global Financial Leadership

The US dollar’s status as the world’s primary reserve currency provides the US with significant economic and political leverage. The advent of digital currencies, particularly those issued by rival powers, could challenge this dominance. By developing a robust and secure digital dollar, the US can proactively defend and strengthen its position, ensuring that the dollar continues to be the preferred medium for international trade and investment in the digital age.

Countering Digital Authoritarianism

Some countries are developing CBDCs with features that could enable greater state surveillance and control over citizens’ financial activities. A US digital dollar, designed with strong privacy protections and democratic values, could offer an alternative model, promoting open and transparent financial systems globally. This ideological competition is a significant aspect of the CBDC landscape, and the design choices for the digital dollar 2026 will send a powerful message about American values.

Facilitating Humanitarian Aid and Sanctions

A digital dollar could also enhance the effectiveness of foreign policy tools. For instance, it could streamline the delivery of humanitarian aid to regions in need, ensuring that funds reach their intended recipients more efficiently and transparently. Conversely, it could also provide more precise tools for implementing sanctions against rogue regimes or individuals, minimizing unintended consequences on innocent populations.

Conclusion: The Future of Money with a Digital Dollar in 2026

The prospect of a digital dollar 2026 represents a pivotal moment in the evolution of money and finance. It holds the promise of a more inclusive, efficient, and resilient financial system, capable of addressing the challenges of the 21st century. From empowering the unbanked to providing the Federal Reserve with enhanced monetary policy tools, the potential benefits are substantial.

However, the journey towards a digital dollar is complex and laden with significant challenges. Issues of privacy, cybersecurity, financial stability, and the potential impact on the commercial banking sector demand careful consideration and robust solutions. The decisions made in the coming years regarding its design, legal framework, and implementation will shape its ultimate success and its role in the global economy.

As we move closer to 2026, the discussions will undoubtedly intensify. It is crucial for policymakers, industry leaders, and the public to engage in informed dialogue, weighing the opportunities against the risks. The successful implementation of a digital dollar could solidify the US’s position as a leader in global finance, foster a new era of financial innovation, and ultimately benefit all Americans by providing a more modern, secure, and accessible form of money. The future of money is digital, and the digital dollar 2026 is set to be a cornerstone of this transformative era.